Are The Rating Agencies Complicit In Another Massive Scandal: A WSJ Investigation Leads To Shocking Questions

Are The Rating Agencies Complicit In Another Massive Scandal: A WSJ Investigation Leads To Shocking Questions

Over the past two years, a key development many bears have been citing as a potential catalyst for a sharp market drawdown (i.e. crash), is the systematic downgrade of billions of lowest-rated investment grade bonds to junk as a result of debt leverage creeping ever high, coupled with the inevitable slowdown of the economy, which would lead to an avalanche of “fallen angels” – newly downgraded junk bonds which institutional managers have to sell as a result of limitations on their mandate, in the process sending prices across the corporate sector sharply lower.

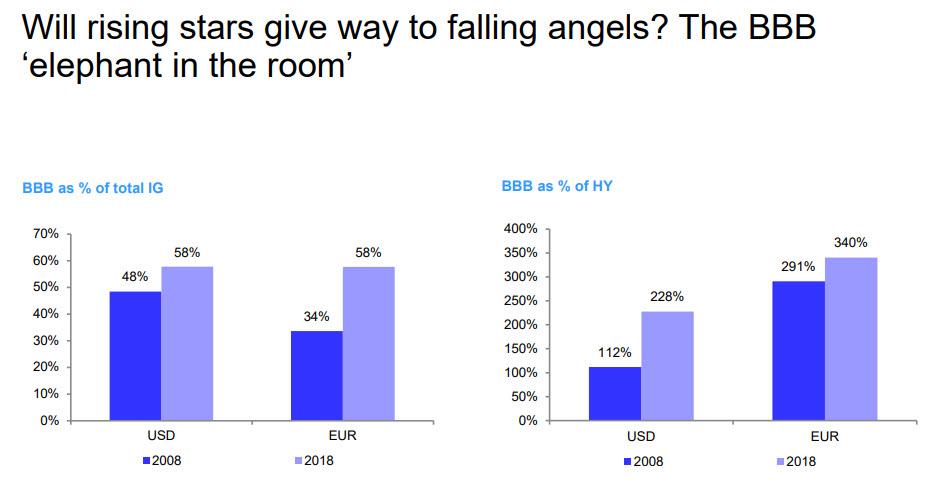

As we discussed in July, the scope of this potential problem is massive, with the the lowest-rated, BBB sector now nearly 60% of all investment grade bonds, and more than double the size of the entire junk bond market in the US, and 3.4x bigger than the European junk bond universe.

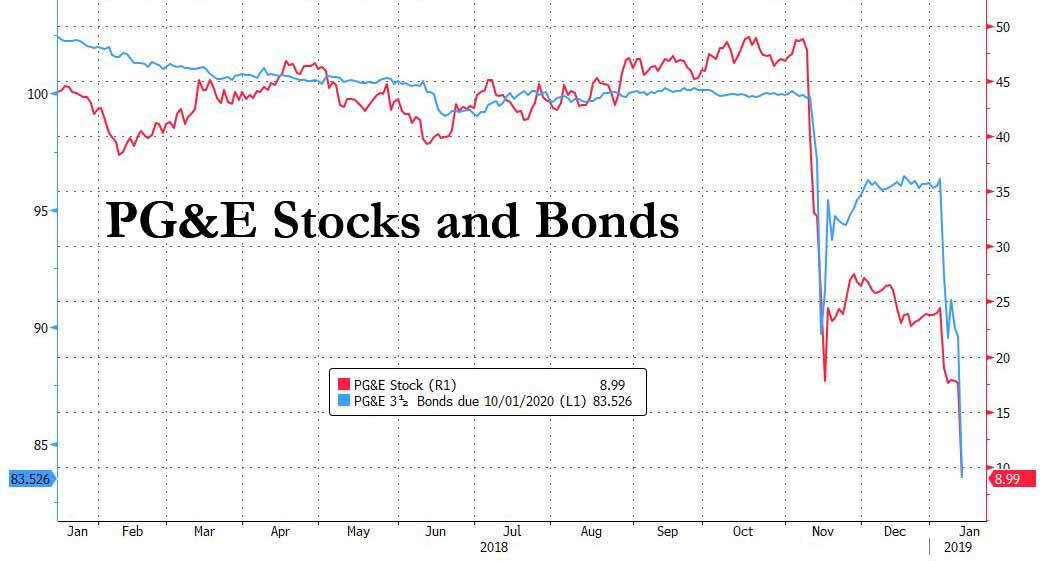

Yet after waiting patiently for years for the inevitable downgrade avalanche which would unleash a zombie army of fallen angels and potentially spark the next crash, with the occasional exception of a few notable downgrades such as PG&E and Ford, this wholesale event has failed to materialize so far, something which the bulls have frequently paraded as an indication that the economy is far stronger than the bears suggest.

But is it? And instead of the economy being stronger, are we just reliving the past where rating agencies pretended everything was ok until the very end, only to admit they were wrong all along, and then slash their rating retrospectively, too late however as the next financial crisis is already raging.

Well, according to a must-read expose by the WSJ, it appears that we are indeed doomed to repeat the mistakes of the past, because as the Journal’s Gunjan Banerji and Cezary Podkul observe, what was supposed to be a 2015 downgrade has dragged on for over 4 years… while the rating agencies appear to be purposefully looking elsewhere.

To wit:

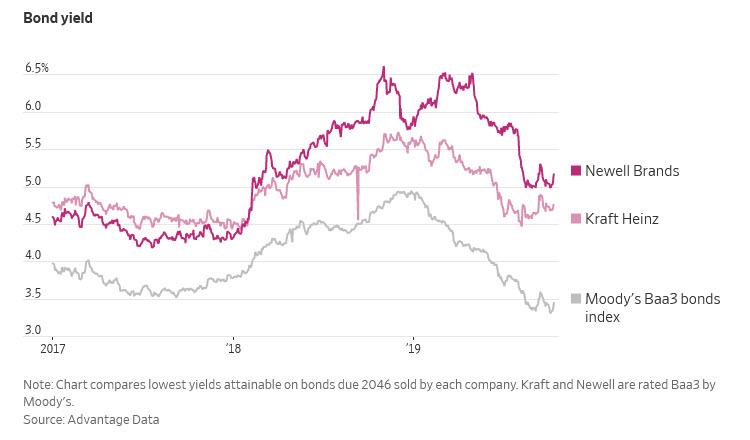

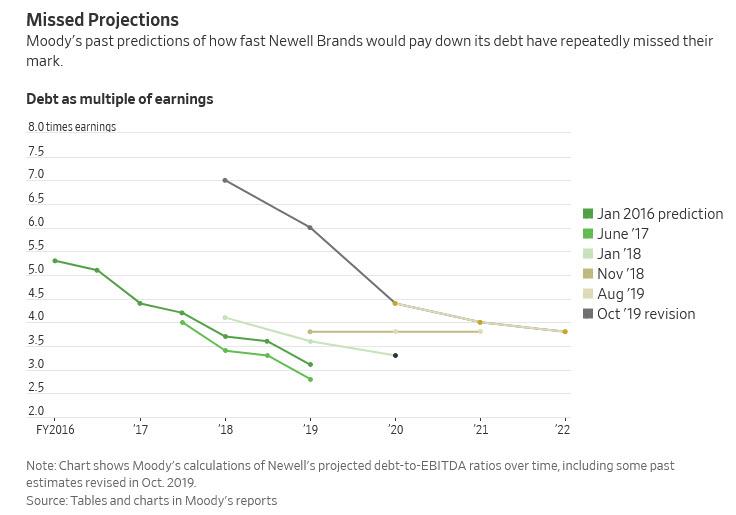

In August, bond-ratings firms Moody’s and S&P Global predicted that Newell Brands would soon reduce its heavy debt load, allowing it to keep its coveted investment-grade bond rating.

They made the same prediction in 2018. And in 2017. And in 2016. And in 2015, when the company announced a big merger that quadrupled its debt. Yet bond ratings for the maker of Rubbermaid containers and Sharpie markers haven’t budged.

Those asking “why not” are correct, and not just because the rating agencies appear to be delaying a moment of reckoning, clearly aware of the shitstorm they would trigger if they downgraded every soon to be “fallen angel” – just like in 2007 with their ridiculous CDO assessments, the raters have made glaring mistakes, which when correct, have still failed to prompt the agencies into action:

When S&P and Moody’s made their upbeat projections in 2018, they made an error that understated Newell’s indebtedness, according to a Wall Street Journal review of the rating firms’ calculations. They have since fixed their numbers, but still rate Newell investment-grade. Investors have been less forgiving, selling off the bonds and driving up their yield.

The raters’ response: “Moody’s and S&P didn’t dispute revising their calculations, but said the changes didn’t affect their ratings.“

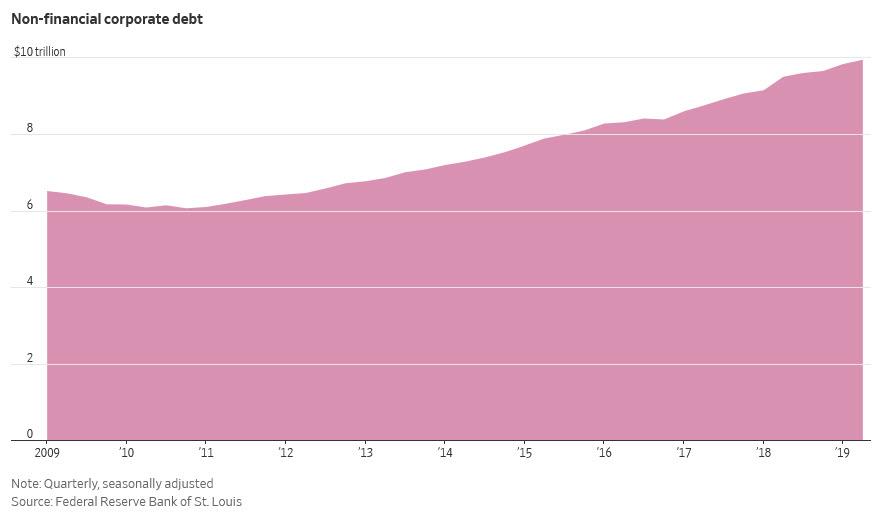

Naturally, it’s not just Newell: amid an epic corporate borrowing spree that sent total non-financial corporate debt to a record $10 trillion…

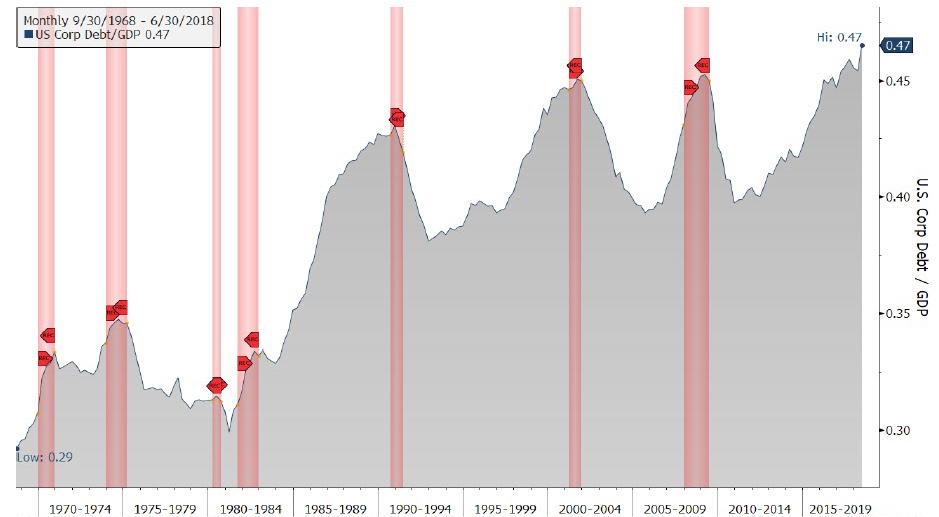

… sending it to the highest percentage of GDP on record…

… ratings firms have given leeway to other giant borrowers like Kraft Heinz, Campbell, and of course, IBM, which recently almost doubled its debt load to fund the purchase of Red Hat, allowing their balance sheets to swell.

“It’s pretty eye-popping if you’ve been doing this for 20-plus years, to see how much more leverage a number of these companies can incur with the same credit rating,” said Greg Haendel, a portfolio manager at Tortoise in Los Angeles overseeing about $1 billion in corporate bonds. “There’s definitely some ratings inflation.”

To veterans it may be “eye-popping” but to everyone else, it’s a surprise, so here it is visualized: the average Investment Grade company has seen its net leverage rise from roughly 2x to over 3x in the past decade, while leverage for the average BBB name has risen by more than 50% from just over 2x to 3.3x in the same time period.

The relentless increase in leverage should not come as a surprise: years of near-zero interest rates (or negative in the case of Europe) have fueled a record boom in borrowing, driving debt owed by U.S. companies (ex banks) to nearly $10 trillion—up about 60% from pre-crisis levels, with a majority of the proceeds then used by companies to repurchase their own stock and lift the company stock price to likewise nosebleed levels. It is certainly not a surprise then, that leverage hit an all time high in Q2 of this year, according to JPMorgan.

The record debt increase has sparked one of “the most divisive debates on Wall Street” as the WSJ puts it: Will higher debt loads cause big losses when the economy turns? Or have low interest rates made the borrowing more manageable? And, as noted above, will the sudden collapse of “fallen angels” when rating agencies can no longer kick the can, unleash the next financial crisis?

In their own defense, Moody’s and S&P say their ratings are “accurate” because companies like Newell have solid, global brands and generate sufficient cash flow to pay off the bonds. “We take rating actions where appropriate in line with our methodologies,” said Tom Mowat, analytical manager at S&P Global Ratings. The ratings firms also say their grades have accurately predicted defaults, which is their main purpose.

What Mowat is really saying, is that since central banks have forced bond investors into anything that offers even a modest yield, the fact that yields on the companies in question have fallen is confirmation the rating agency is right.

That, of course, is bullshit: what is really happening is unprecedented herding of the investing community, and even though there is a tsunami of capital chasing even the most modest return, events such as PG&E still happen which reprice bonds from par to a fraction of their value overnight as the folly of “investment grade” fundamentals is laid bare for all to see.

There is another, unspoken reason why S&P and Moody’s have dreaded downgrading names such Newell, Kraft and Campbell Soup, all of which are triple-B rated, the lowest category for bonds considered investment-grade, which is what countless vanilla funds are only allowed to hold: a mass downgrade to high yield, or junk, would result in forced liquidation and an unprecedented repricing of the junk bond market, not to mention raising the newly downgraded companies’ borrowing costs.

Amid the debt issuance spree of the past decade, the triple-B rating has exploded in the last decade, with debt outstanding more than tripling to $3.7 trillion, more than double the size of the entire US junk bond universe. Should a substantial fraction of these companies be downgraded, it would result in an unprecedented shockwave. These days, more than 50% of all investment-grade bonds are rated triple-B, up from 38% in September 2009.

To be sure, some investors still remember what happened when they put their trust in rating agencies, and despite their BBB-rating, over $100 billion worth of bonds already trade with yields like junk despite their triple-B-minus ratings, despite the flood of cash into investment-grade debt.

Which brings us to the real reason why rating agencies are loath to downgrade most of these “pre-fallen angles” to their true, junk status: such a move would validate what is arguably one of the most bearish catalyst of the past few years, potentially triggering the next market crash. Which, of course, makes the raters even more unwilling to rate these credits at fair value, because the longer they delay admitting reality, the greater the price to pay will be in the end. Which leaves them paralyzed, and pretending that a 3.5x leverage now for a BBB-rated company is the same as a 2.0x levereage at the start of the decade.

Meanwhile, investors and analysts have told the SEC that they are concerned about the buildup of triple-B debt. Here are some examples from the WSJ:

Last October, Adam Richmond, Morgan Stanley’s then head of U.S. credit strategy, testified at an SEC hearing that if leverage were the sole criteria for ratings, many triple-B rated companies wouldn’t qualify for such high grades. He warned that “downgrade activity could be heavy” once the economy inevitably weakens. The firm’s analysts wrote in a September report that investment-grade companies “have not de-levered significantly and are still getting credit for assumed earnings growth, integration of acquisitions, and other ‘plans’ to delever.”

JPMorgan raised similar concerns in a report it submitted to a bond-investor advisory committee at the SEC. In February, the committee created a new group to examine credit ratings and potentially recommend new regulations to boost oversight of the industry, according to people familiar with the group

So far, regulators like rating agencies, have decided to simply stick their head in the sand, and hope that this, too, shall pass. It won’t.

Meanwhile, as Moody’s and S&P desperately scramble to defend their reputation before their criminal inactivity is seen as the catalyst for the next crash, arguing that cash flow has actually improved in recent year (spoiler alert: it hasn’t), even the IMF’s new head, Kristalina Georgieva, said last month that $19 trillion of corporate debt would be at risk of default, nearly 40% of total debt in eight major economies. “This is above the levels seen during the financial crisis,” she said.

But wait, it gets better. Instead of downgrading companies on the cusp of being junk-rated, last year S&P actually upgraded Kraft, one of the biggest corporate borrowers, saying cost savings would help push leverage below four times annual earnings by late 2019. Then, in June, following the company’s humiliating earnings restatement which embarrassed even crony capitalism market wizard, Warren Buffett, S&P had no choice but to downgrade Kraft … but it still kept Kraft at the lowest rung of investment-grade, giving it another two years to meet the target. In September, S&P estimated leverage was in the “high-4x area.” Since then, Kraft’s leverage has risen even more.

“How long do you give management the benefit of the doubt?” said Lon Erickson, a portfolio manager at Thornburg Investment Management, who oversees $7 billion in corporate debt, including some Kraft bonds.

Here we’ll paraphrase Lon, and ask: how long will this Kabuki farce, in which everyone knows that the rating agencies are desperate not to be blamed for the next crisis – for not doing their job again – and thus will never downgrade trillions in BBB-rated bonds to junk, continue?

Apparently the answer is “for a long time.” Another example:wWhen Keurig Green Mountain merged with Dr Pepper Snapple Group in 2018, Moody’s said it could downgrade the combined company if leverage didn’t fall to about four times earnings by January 2020. This year, Moody’s said four times annual earnings by the end of 2020 was fine.

“If it’s a strike, it’s a strike. If it’s a ball, it’s a ball,” said Joe Pimbley, a former Moody’s analyst and principal of Maxwell Consulting. “Call it as you see it.”

If only his former co-workers would do that. Instead, they are doing what they did in the run up to the last financial crisis – lying.

The ratings firms say they question companies’ debt reduction plans. “By nature we are a pretty skeptical bunch. We like to poke holes in stories,” said Peter Abdill, who oversees Moody’s ratings for consumer products companies.

No, you are not a skeptical bunch. You are a bunch of pathological liars and hoping that by the time the system comes crashing down, you will have quit long ago, making your criminal inactivity someone else’s problem. Meanwhile, the rating agencies are engaging in what appears to be borderline criminal behavior, only when pressed, they will simply say “it was a mistake.” Take the example of Newell:

One company that has been given significant leeway by ratings firms is consumer goods giant Newell Brands, which makes everything from Elmer’s glue to Yankee Candles. While food companies like Kraft and Campbell produce steady earnings in good and bad economies, Newell is more cyclical, meaning it is more likely to run into trouble during a downturn. When Newell said it would acquire rival Jarden Corp. for about $20 billion in December 2015, S&P and Moody’s analysts said Newell could keep its low investment-grade rating because debt would fall from more than five times projected earnings to under four times by December 2017.

Newell had tens of millions of dollars riding on that decision. A provision tucked into an $8 billion acquisition bond sale in March 2016 said Newell would owe its investors as much as $160 million more in annual interest costs if it got downgraded into junk territory.

As an aside, the provision highlights the conflict faced by the ratings firms. While investors use rating firms’ research, it is the companies that issue bonds who pay for the ratings. And while Moody’s and S&P say they don’t allow the conflict, or bond provisions like these, to influence their rating decisions, it’s beyond obvious that there is no objectivity left when rating BBB-rated companies:

But we digress, back to the story of Newell:

In 2018, under pressure from activist investors, Newell announced plans to sell about a third of its businesses and buy back more than 40% of its shares, moves that could slow down deleveraging. Moody’s and S&P confirmed the company’s rating and predicted its leverage would fall to less than four times earnings by the end of 2018.

This past February, Newell announced that its debt was 3.5 times earnings at the end of 2018. But Newell failed to account for lost earnings from businesses it sold when it calculated the figure. Investors were skeptical, said James Dunn of CreditSights, an independent credit research firm. He estimated Newell’s actual debt load to be 5.3 times projected earnings.

Of course, Moody’s and S&P’s leverage estimates mirrored Newell’s erroneous approach, the WSJ said after reviewing their calculations. Moody’s estimated Newell’s year-end leverage at 3.8 times in a Nov. 2018 report. S&P put it at 3.9 times in a July 2018 note. Worse, Moody’s also overstated Newell’s earnings by double-counting amortization when calculating EBITDA.

Adjusting for the errors, Moody’s estimate of Newell’s leverage should have been closer to 6x earnings, the Journal found. Instead, Moody’s currently has it below 4.0x! For those confused, leverage around 6x EBITDA would – in a normal world – make the company a Jefferies special: somewhere in the B2/B category.

Having been caught in a flagrant mistake, earlier this month, Moody’s updated its calculation of Newell’s year-end 2018 leverage to six times earnings, versus a revised estimate of 5.5 times it published in August that took various asset sales into account. However, it sees that number drifting as low as 3.8x by 2022. S&P raised its number to 5.4 times earnings, citing “normalized” figures that also took into account Newell’s asset sales.

End result? The company is still investment grade. An S&P spokesman said in an email that “our analysis speaks for itself.”

It does indeed, and when the next crisis hits, everyone will remember precisely what your “analysis” spoke.

Tyler Durden

Mon, 10/21/2019 – 17:32

![]() Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/2_M-Sa5-3Bc/are-rating-agencies-complicit-another-massive-ratings-scandal-wsj-investigation-leads

Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/2_M-Sa5-3Bc/are-rating-agencies-complicit-another-massive-ratings-scandal-wsj-investigation-leads