Don’t Be Fooled By The Oil Price Rebound

Authored by Irina Slav via OilPrice.com,

A mild winter in the northern hemisphere, the COVID-19 outbreak, and now the price war that Saudi Arabia declared last weekend have combined to produce an all-new oil price crisis just four years after the last one. And things might get worse before they get better.

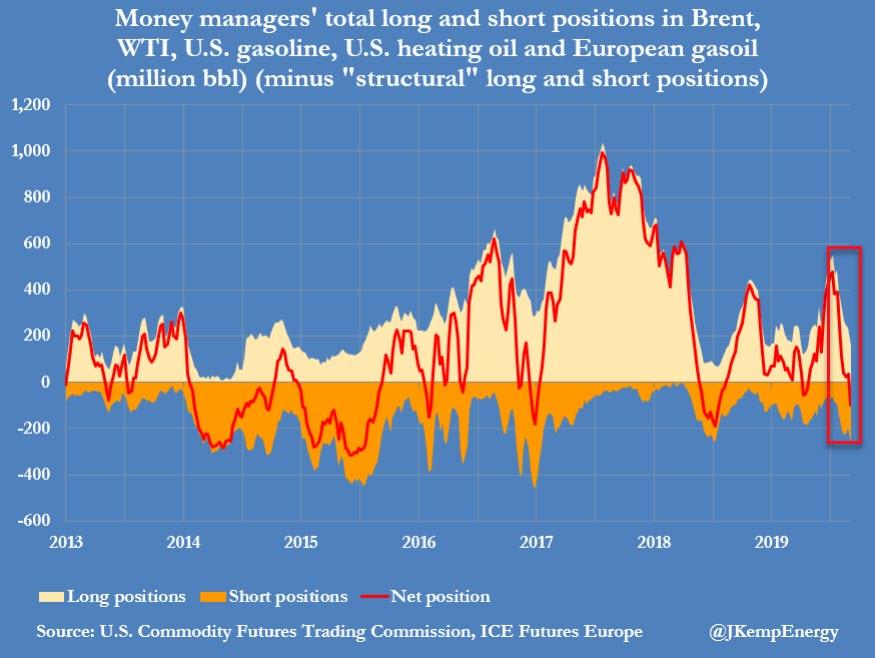

After last week data from hedge funds showed a slowdown in the selloff of oil and fuel contracts, as reported by Reuters’ John Kemp, this week’s data, for the first week of March, indicated a serious acceleration of sales. During that week, Kemp reported in his weekly column, fund sold the equivalent of 133 million barrels of oil across the six most traded oil and fuel contracts. This compares with sales of just 11 million barrels of oil equivalent across the six contracts just a week earlier.

The overall long position of hedge funds on oil and fuels was down to 392 million barrels by March 3, Kemp also noted, which compares with 970 million barrels at the start of 2020. That’s a decline of as much as 60 percent, and that’s not all. The ratio of bullish to bearish positions, Kemp says, has fallen to 2:1 from 7:1 in January and is one of the lowest ratios in the past few years.

Meanwhile, the COVID-19 epidemic is marching across the world, fueling panic and dampening oil demand as people self-quarantine, flights get grounded, Italy extends its lockdown to the whole country, and a growing number of states in America declare a state of emergency.

While this was happening, Saudi Arabia fired the first shot in what many are seeing as an all-out price war. After Russia refused to take part in deeper production cuts to prop up prices, with energy minister Alexander Novak saying that from April the country’s oil producers will be pumping oil as usual, without compliance to any OPEC+ quotas, Riyadh said it was cutting the prices for its oil and planning a production increase, utilizing its full production capacity, which is about 12 million bpd.

The bad news: hedge funds were extremely bearish on oil and fuels even before OPEC+ broke down.

This suggests they might get even more bearish on oil after the latest developments there. And this, in turn, means prices could fall further despite a temporary improvement yesterday, in which Brent recouped some of its losses to trade, at the time of writing, at close to $37 a barrel.

“This has turned into a scorched Earth approach by Saudi Arabia, in particular, to deal with the problem of chronic overproduction,” John Kilduff from Again Capital told CNBC.

“The Saudis are the lowest cost producer by far. There is a reckoning ahead for all other producers, especially those companies operating in the U.S shale patch.”

“The prognosis for the oil market is even more dire than in November 2014, when such a price war last started, as it comes to a head with the significant collapse in oil demand due to the coronavirus,” Goldman Sachs’ Jeffrey Currie said. The investment bank cut its oil price forecast for the second and third quarter to $30 a barrel for Brent, noting that the benchmark could dip even lower, into the $20s.

The situation in oil looks like a three-person staring contest. With low-cost producer but ambitious spender Saudi Arabia on one side, pumping at will, Russia on the other, braced for lower prices and its previous experience with price crashes, and US oil producing companies on the third side, grappling with insufficient cash for dividends and, for many shale producers, a heavy debt burden. For now, the analyst consensus seems to be that U.S. shale independents will be the ones to blink first.

Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/KLjY3XA8zOI/dont-be-fooled-oil-price-rebound