FX Volatility Nears All Time Low In “Perfect Storm Of Vol, Skew And Carry”

FX Volatility Nears All Time Low In “Perfect Storm Of Vol, Skew And Carry”

While the VIX still has a fair ways to go before it plumbs the all-time single-digits lows that defined the spectacularly serene equity markets in 2017, FX vol is already there: the JPMorgan Global FX volatility index has dropped to 6 year low levels, and is just shy of all time lows.

Of course, most of this stability in the FX realm is due to central banks depressing cross-asset vol; yet the more vol is pushed lower, the higher it will spring back once central banks lose control; as such it is only a matter of time before buying FX vol is a winning trade.

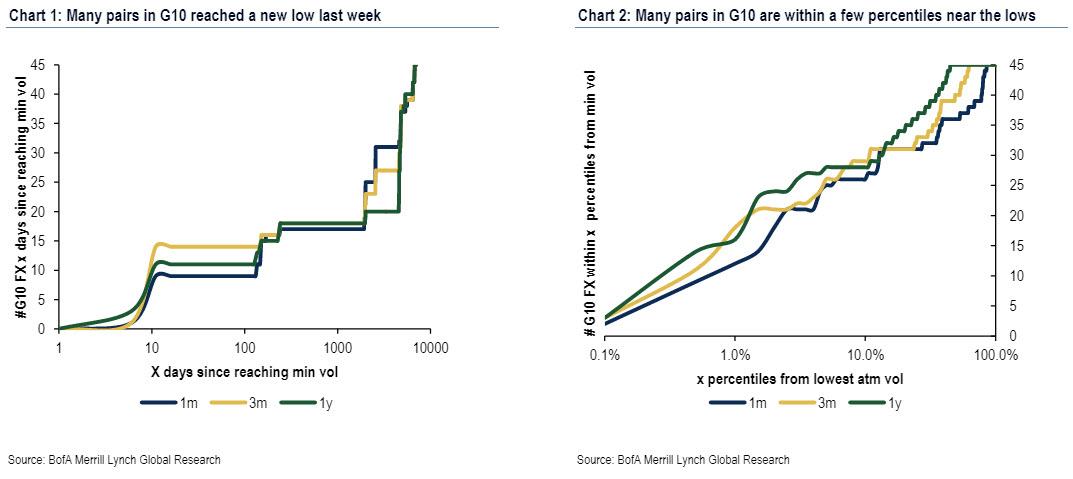

Commenting on this record low FX vol and currency-specific volatility, BofA’s Vadim Iaralov writes that a “dozen FX vols reached new lows last week and most remain close to their all-time lows” in what he calls a “perfect storm of vol, skew and carry.”

Some more details from the BofA FX strategist:

A number of G10 vols have already made new lows last week including nine pairs in G10 of one-month ATM vols, 14 pairs of three-month vol and 11pairs of one-year. Current vols remain low at 1st percentile or lower including 12 pairs of one-month vols, 18 pairs of three-month vols and 16 pairs of one-year vols.

His obvious conclusion: the low vol offers attractive hedging opportunities, especially for investors concerned about against USD gains.

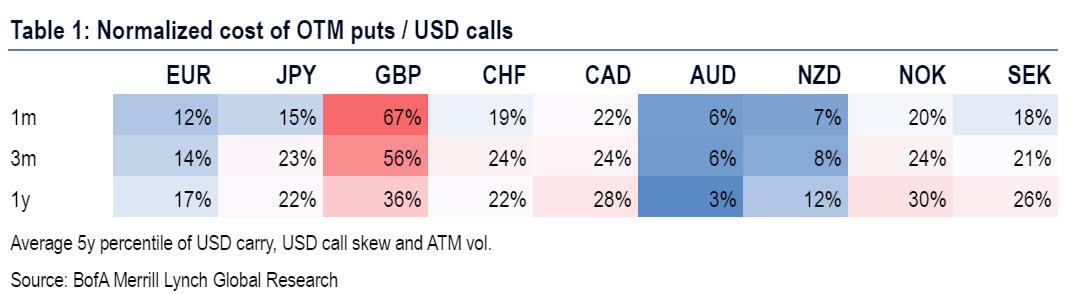

Looking at the dollar alone, in addition to low ATM vols, Iaralov points out that USD call skew is also near historically flat and USD carry remains positive, if somewhat diminished after recent Fed cuts.

FX traders can combine these measures to normalize cost of out-of-the-money options; BofA has done so, and found that out-of-the-money puts on AUD, NZD and EUR are especially attractive, offering topside USD hedges at a historically low cost. By contrast, GBP, NOK and CAD hedges are less affordable. Given Brexit and the UK election ahead, 1m GBP hedges via OTM puts are especially pricey.

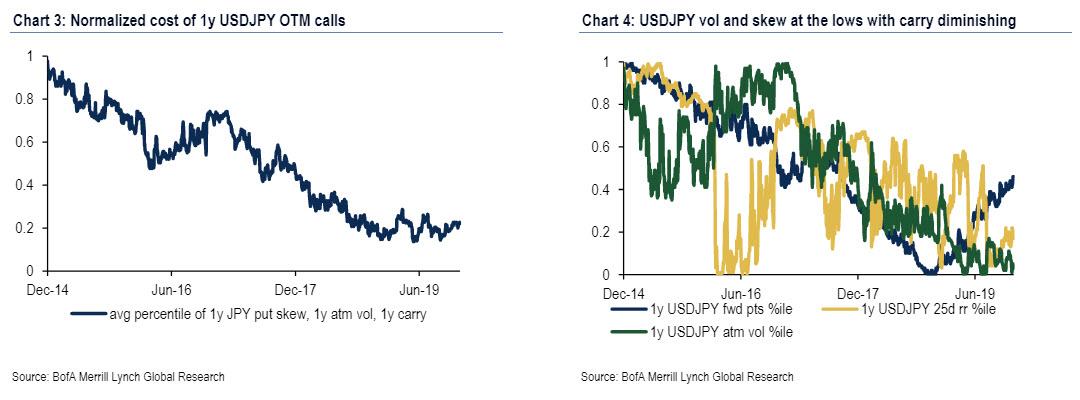

In addition, recent JPY gains have cheapened OTM USD/JPY calls of fixed strikes, for example for corporates restructuring existing hedges. As Iaralov adds, the front-end 1m USDJPY benefits from a confluence of attractive vols, skew and carry. However, at the 1y mark the carry has turned less beneficial, pricing in another Fed cut, even though the vols and USDJPY skew are near the lows.

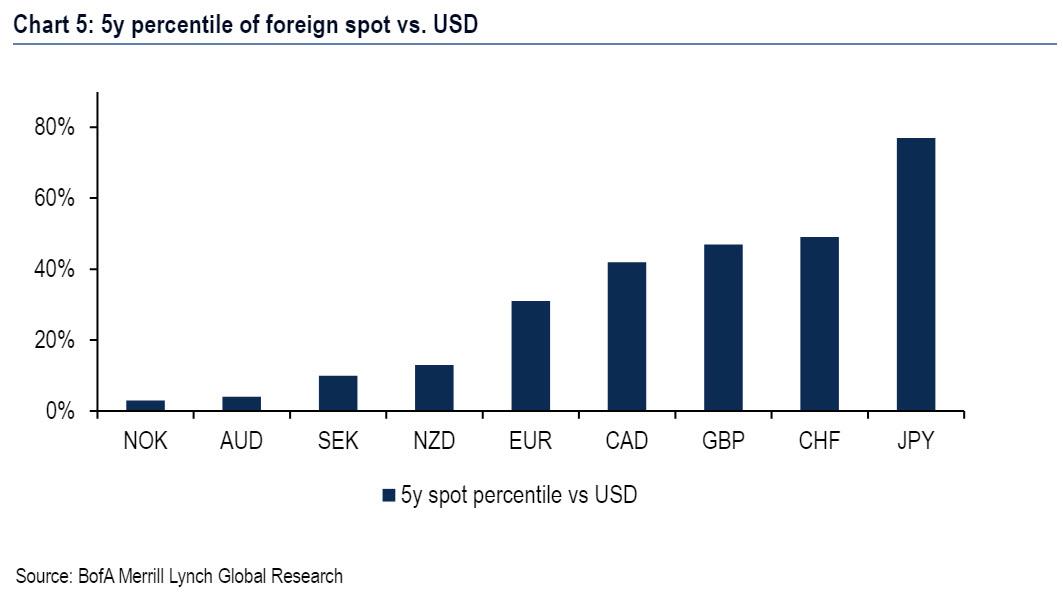

Finally, when constructing low vol hedging trades, keep in mind that spot levels can be incorporated when considering the cost of options struck at specific, fixed strikes rather than in delta terms. OTM USD calls at fixed strikes are cheaper when USD/FX is weaker as it is for USD/JPY and more expensive for USD vs NOK and USD vs AUD.

Tyler Durden

Fri, 12/06/2019 – 13:20![]() Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/9AD4z427-t0/fx-volatility-nears-all-time-low-perfect-storm-vol-skew-and-carry

Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/9AD4z427-t0/fx-volatility-nears-all-time-low-perfect-storm-vol-skew-and-carry