Global Markets Soar After China Hints At Trade Talk Optimism

It is a sea of green across global markets as European stocks and US equity futures rallied sharply and Asian shares pared earlier declines, after after comments from China that Beijing is in “effective contact” with the US on trade and that they are discussing the upcoming September talks. The Chinese Yuan soared while Treasury yields jumped.

The bullish sentiment emerged after China’s Commerce Ministry spokesman Gao Feng said that both US and China trade teams have been in touch, adding that China has ample retaliatory measures and are lodging solemn representations with the US over the additional tariffs, both sides are discussing the September talks and if China officials go the the US then there should be an environment created for progress in the negotiations; calls on the US to cancel the planned additional tariffs to avoid a trade war escalation.

As a result, S&P 500 contracts turned sharply higher, rising 0.7% alongside the 1% move higher in Stoxx Europe 600 Index, just around 3am when China’s commerce ministry spokesman said escalating the trade war won’t benefit either side, and that it was more important to discuss removing the extra duties.

The comments had come after a choppy Asian session. MSCI’s broadest index of Asia-Pacific shares outside Japan fell 0.15%, Singapore shares hit eight-month lows and Japan’s Nikkei ended fractionally lower.

European bourses are trading at session highs in-spite of a relatively lacklustre open, thanks to the Chinese comments. However, while the market reaction does not reflect this there were some less positive comments as well particularly that China has ample retaliatory measures. Looking ahead, on the US-China front markets are largely awaiting an update on the timeline for Septembers talks. Returning to Europe, the FTSE MIB is the notable outperformer (+1.9%) as the bourse derives strength from the increasing prospect of an Italian coalition forming and thus the budget passing. Similarly to the indices, sectors are all in the green with no notable under/outperformer.

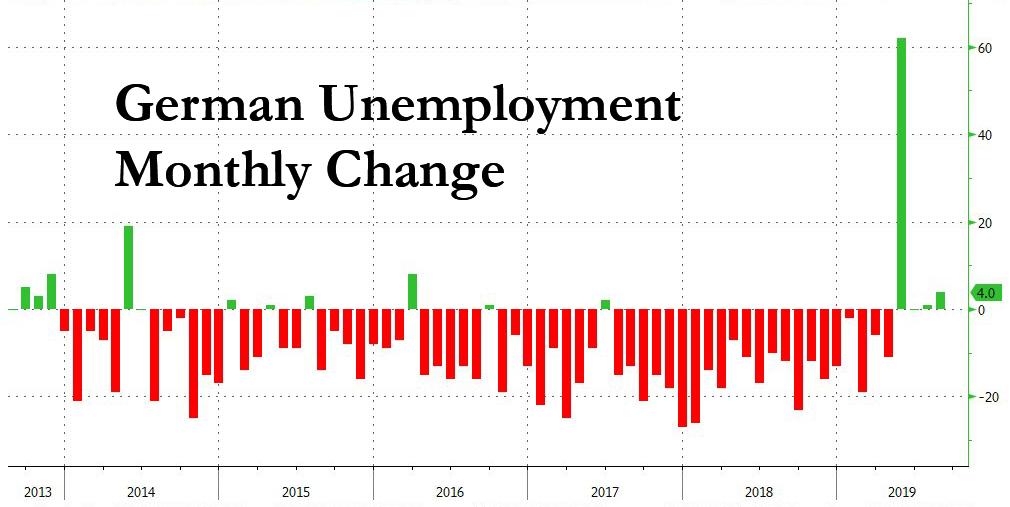

Markets aside, the European economy was hit again as Germany’s labor market looks like it’s starting to crack under the weight of a manufacturing recession, raising the pressure for the government to respond with fiscal stimulus. The number of people out of work increased by 4,000 to 2.29 million in August, the fourth straight month that joblessness failed to drop after six years of almost continuous decline. The unemployment rate remained at 5%, near a record low.

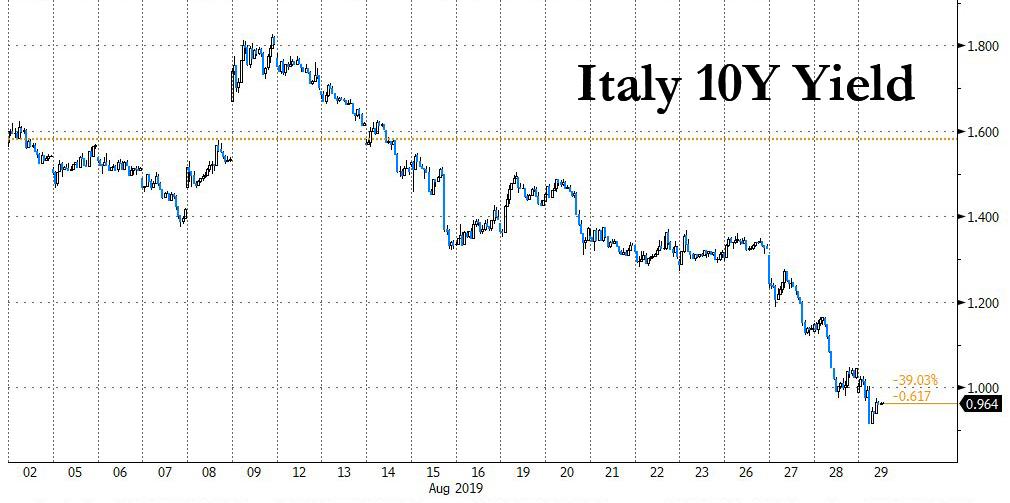

Most European and U.S. government bond yields traded higher on the back of this improved risk sentiment, with BTPs a notable exception. Italian bonds added to the impressive rally in recent days as a new government looks like it will be formed. 10-yr BTP yield trades at record low of 0.93%. That was after the country’s 5-Star Movement and opposition Democratic Party said they would try to form a coalition, setting aside years of hostility to avert a snap election and the economic uncertainty that comes with it.

The two sides still need to agree on a shared policy platform and a team of ministers, but 5-Star chief Luigi Di Maio and his PD counterpart Nicola Zingaretti said they had pledged to find common ground for the good of the country. “We love Italy and we consider it worthwhile to try this experience,” Zingaretti told reporters. Speaking shortly afterwards, Di Maio said: “We made commitments to the Italians…and come what may we want to fulfil them.”

The 10-year Japanese government bond yield had dipped 1 basis point to minus 0.285% overnight too, which is just above its record low of minus 0.300% touched in 2016.

“Falls in global bond yields reflect growing concerns that long-term global growth is slowing down on U.S.-China tensions and worries over subsequent global supply chain disruptions,” said Tomoo Kinoshita, global market strategist at Invesco Asset Management in Tokyo. “Stock markets on the other hand are supported in the near-term by hopes of more stimulus, notably from the Federal Reserve and the European Central Bank,” he said.

Reflecting underlying nervousness, the Merrill Lynch move index, a gauge of investors’ expectations on how volatile U.S. bonds will be, has risen back near three-year highs marked earlier this month.

In FX, there was little reaction from the euro but there was barely any currency market action generally. The Bloomberg USD index was little changed, with CAD leading G-10 gain, NOK lagging, but most G-10 pairs trade in tight ranges. The Japanese yen was a touch higher heading for its biggest monthly rise since May, while sterling was flirting with a January 2017 low of $1.2015 against the dollar after Prime Minister Boris Johnson’s plan on Wednesday to suspend Britain’s parliament increased no-deal Brexit nerves.

China’s yuan initially dipped for an 11th straight session although a firmer-than-expected central bank fixing for the 7th session helped stem deeper losses and against a basket of currencies. The People’s Bank of China set its daily fixing at 7.0858 per greenback, stronger than the average estimate of 7.1085 from a survey of 20 traders and analysts. As a result, the Bloomberg replica of the CFETS RMB Index, which tracks the yuan versus a basket of trading partners’ currencies, rose for the first time in week. However, the far sharper move for the yuan took place in afternoon trading when the currency reversed a drop against the dollar, rising as much as 0.3%, after China signaled it wouldn’t immediately retaliate against the latest U.S. tariff increase announced by President Donald Trump last week.

The MSCI emerging market currency index was also at its lowest levels since mid-November, having fallen 0.9% so far this week and set for its biggest monthly fall in more than seven years. The latest hit came in Argentina as it said it wanted to restructure a large chunk of its bonds by extending their maturities and to “re-profile” the maturities of debt owed to the IMF under a $57 billion standby agreement. The battered peso took another hammering on Wednesday, even though the central bank intervened heavily in the foreign exchange market for a second consecutive day.

Argentine assets have been slammed since business-friendly President Mauricio Macri was trounced in primary elections by centre-left Peronist challenger Alberto Fernandez: “President Macri instructed me to solve the short-term problem to guarantee electoral stability, but also in the medium- and long-term so as not to leave a problem for the person who follows, be it he or another candidate,” Argentina’s Treasury Minister, Hernan Lacunza, said.

In geopolitical news, Iran’s Foreign Minister Zarif said it will not be possible for Iran to engage with US unless they stop imposing a war and conducting economic terrorism, while he added the US must observe 2015 nuclear deal if it wants to meet for talks. Elsewhere, Turkey President Erdogan spoke with US President Trump via telephone regarding latest developments in Syria and bilateral issues, while Erdogan said he is in agreement with US which is a correct step towards ‘safe zone’ in northeast Syria. In other news, Russia and Turkey are considering creating a new fighter jet, according to Russian officials.

In commodities, WTI edges slightly higher ($56.07) while Brent slips slightly lower. Precious metal investors were still on a quest to buy safer assets: gold rose as high as $1,543 per ounce, near six-year highs of $1,556.1 set earlier in the week, while silver rose 1.2% to $18.55 per ounce which is just shy of a 2017 peak of $18.65 an ounce.

Market Snapshot

- S&P 500 futures up 0.6% to 2,907.25

- STOXX Europe 600 up 0.7% to 375.61

- MXAP down 0.01% to 151.08

- MXAPJ up 0.2% to 488.03

- Nikkei down 0.09% to 20,460.93

- Topix down 0.01% to 1,490.17

- Hang Seng Index up 0.3% to 25,703.50

- Shanghai Composite down 0.1% to 2,890.92

- Sensex down 0.5% to 37,257.04

- Australia S&P/ASX 200 up 0.1% to 6,507.40

- Kospi down 0.4% to 1,933.41

- German 10Y yield rose 2.0 bps to -0.694%

- Euro up 0.01% to $1.1079

- Brent Futures down 0.2% to $60.36/bbl

- Italian 10Y yield fell 9.2 bps to 0.702%

- Spanish 10Y yield rose 2.7 bps to 0.092%

- Brent Futures down 0.2% to $60.36/bbl

- Gold spot up 0.1% to $1,540.74

- U.S. Dollar Index up 0.03% to 98.24

Top Overnight News

- British Prime Minister Boris Johnson’s move to suspend parliament and come good on his promise to avoid any more delays to Brexit has set the clock running for his opponents to thwart him; the question is whether they can do it in time

- The Trump administration is giving careful thought to selling something Wall Street may not be ready to buy: ultra-long debt. Treasury Secretary Steven Mnuchin said that offering bonds with maturities of 50 to 100 years is under “very serious consideration,” with officials conducting an intensive review

- President Sergio Mattarella tapped Giuseppe Conte, Italy’s outgoing prime minister, to iron out the differences between the Five Star Movement and the center-left Democratic Party and form a working coalition that can overcome the groups’ longstanding differences

- Germany’s labor market looks like it’s starting to crack under the weight of a manufacturing recession, raising the pressure for the government to respond with fiscal stimulus

- China’s economy slowed further in August as weak domestic conditions, intensifying tensions with the U.S. and worsening global trade all combined to undermine the outlook

- Mnuchin said U.S. trade officials expect Chinese negotiators to visit Washington, but wouldn’t say whether a previously planned September meeting would take place. He also said U.S. doesn’t intend to intervene on dollar for now

- Italy’s acting prime minister Giuseppe Conte will be tasked with forming a government supported by the Five Star Movement and the Democratic Party, two long-time rivals who have little more in common

- Argentina’s government is seeking to extend maturities on tens of billions of dollars of debt and delay repayments to the IMF after a collapse in the peso and its bonds

- BOJ board member Hitoshi Suzuki stressed the need for caution about further monetary stimulus as other global central bankers act to counter an economic slowdown

- Low inflation means the U.S. central bank can let a hotter economy draw more people into the labor force, San Francisco Fed President Mary Daly said

Asian equity markets traded mostly lower after failing to sustain the positive, but quiet lead from their counterparts in the US where energy outperformed and the DJIA led the majors higher to reclaim 26000. ASX 200 (+0.1%) and Nikkei 225 (-0.1%) were subdued with focus in Australia centred on earnings including Woolworths. Nonetheless, the downside for the broader market was limited amid gains in mining names with gold lifted by a mild safe-haven bid and after the energy complex benefitted from the recent bullish inventory data, while the Japanese benchmark gave up initial gains after succumbing to the weight of the flows into JPY. Hang Seng (+0.4%) and Shanghai Comp. (-0.1%) were also lacklustre after PBoC inaction resulted to a drain on liquidity and as China plans tighter regulations on share pledging, as well as to reduce risks for small and medium banks. The losses in Hong Kong have also been a function of weak earnings releases including China Construction Bank which was the first of the Big 4 to report and slightly missed on its FY net. Finally, 10yr JGBs received a lift from the downbeat risk tone and after similar advances of their counterparts in US where there was a strong 5yr auction and the yield inversion briefly widened again, while stronger 2yr JGB auction results also added to the upside.

Top Asian News

- BOJ’s Suzuki Signals More Caution Toward Additional Stimulus

- H.K. Police Confirm Ban on Saturday Protest March

- China’s Policy Bank Bonds Fall as Banks Face New Restrictions

European bourses are at present firmly in the green [Euro Stoxx 50 +1.4%] in-spite of a relatively lacklustre open, until comments from China’s Commerce Ministry that the US and China sides have been in touch and that they are discussing the upcoming September talks sparked a general improvement in risk sentiment. However, while the market reaction does not reflect this there were some less positive comments as well particularly that China has ample retaliatory measures. Looking ahead, on the US-China front markets are largely awaiting an update on the timeline for Septembers talks. Returning to Europe, the FTSE MIB is the notable outperformer (+1.9%) as the bourse derives strength from the increasing prospect of an Italian coalition forming and thus the budget passing. Similarly to the indices, sectors are all in the green with no notable under/outperformer. In terms of individual movers, Micro Focus (-22.4%) are at the bottom of the table after cutting their FY19 outlook. At the other end of the spectrum are Eurofins Scientific (+7.4%) and Bouygues (+5.6%) both post earnings where the latter also confirmed their FY19 targets. Elsewhere, UBS (+1.6%) are supported after hiring Iqbal Khan, a former Credit Suisse executive.

Top European News

- Japan’s DIC Corp. to Buy BASF’s Pigments Unit for $1.1 Billion

- Italy Gives ‘Mr. Nobody’ Second Shot at Forging Stable Coalition

- Ajax Shares Rise After Win Secures Champions League Group Spot

- Miners and Steelmakers Jump After China’s Soft Tone on Trade

In FX, the broad Dollar remains mixed and rangebound, with the DXY still floating above 98.000 amidst relatively benign month end selling signals for portfolio rebalancing countered by weakness/underperformance in currency counterparts. However, risk sentiment in general has been boosted by latest updates from China’s Ministry of Commerce confirming that trade teams from Beijing and Washington have been conversing and face-to-face talks in the US next month are contingent on the right atmosphere to nurture constructive negotiations. The index is currently hovering just shy of 98.322 vs 98.156 at one stage.

- AUD/CAD/NZD – All now firmer than their US peer having underperformed prior to the aforementioned US-China trade update, with the Aussie paring losses post an unexpected drop in Q2 Capex and the Kiwi rebounding from lows hit in the aftermath of ANZ’s August business sentiment survey showing a further deterioration in already weak morale, as expectations fell below zero. Similarly, the Loonie has rebounded from worst levels alongside the Yuan and now eyeing Canadian data for some independent impetus later (Q2 current account and June average earnings). Aud/Usd, Nzd/Usd and Usd/Cad currently around 0.6745, 0.6345 and 1.3285 vs circa 06715, 0.6305 and 1.3320 at the other extremes.

- CHF/JPY/GBP/EUR – In stark contrast to the recoveries noted above, safe-haven unwinding has pushed the Franc and Yen down further from their recent peaks, with Usd/Chf and Usd/Jpy nudging up towards 0.9850 and 106.35, and the latter through 10/21 DMAs in the 106.20-21 area that could be pivotal from technical perspective. Meanwhile, the Pound is straddling 1.2200 following all the midweek drama in Whitehall and the Euro is weighing up softer Eurozone inflation against firmer GDP and mixed sentiment indicators with little reaction/traction via confirmation that Italy’s Conte has been given the mandate to try again as PM, albeit in charge of a different coalition. Indeed, Eur/Usd has slipped a fraction deeper below 1.1100, but holding above bids seen at 1.1050 and ahead of the 2019 low (1.1027).

- EM – Although risk appetite has improved overall, pre-long holiday weekend and early positioning for the final trading session of August appears to be taking its toll on the Turkish Lira, while the Argentine Peso seems destined to come under even more pressure after the Government unveiled its debt rescheduling plan. Usd/Try hovering just under 5.8300 at present and Usd/Ars closed at 57.9400 for reference.

In commodities, WTI and Brent are in positive territory thus far, with the complex recovering somewhat from the downturn in sentiment overnight on this mornings aforementioned US-China updates. Specific newsflow for the complex has been light, though recent reports have indicated that the Adrian Dary is unloading its crude cargo in Turkey. Turning to metals, where spot gold remains comfortably above the USD 1500/oz mark but has drifted somewhat in-line with the improvement in risk sentiment thus far; to a session low of USD 1536/oz. Conversely, copper prices have derived considerably upside from the risk-on tone though prices remain constrained by the USD 2.60 mark.

US Event Calendar

- 8:30am: Wholesale Inventories MoM, est. 0.15%, prior 0.0%

- 8:30am: GDP Annualized QoQ, est. 2.0%, prior 2.1%

- 8:30am: Core PCE QoQ, est. 1.8%, prior 1.8%

- 8:30am: Advance Goods Trade Balance, est. $74.4b deficit, prior $74.2b deficit, revised $74.2b deficit

- 8:30am: Retail Inventories MoM, est. 0.3%, prior -0.1%, revised -0.3%

- 8:30am: Personal Consumption, est. 4.3%, prior 4.3%

- 8:30am: Initial Jobless Claims, est. 214,000, prior 209,000; Continuing Claims, est. 1.69m, prior 1.67m

- 10am: Pending Home Sales MoM, est. 0.0%, prior 2.8%; YoY, est. 1.8%, prior -0.6%

DB’s Jim Reid concludes the overnight wrap

A memorable date today for me for two reasons. Firstly, 25 years ago on this day one of the most important albums in my life was released – namely “Definitely Maybe” by Oasis. Time flies. It shaped my final year at university and the next few years thereafter. There aren’t many better songs than “Live Forever” or “Slide Away.” Secondly, two years ago an event occurred that shaped my life in a much more challenging way and I’m fortunate it didn’t send me down the path of “Cigarettes and Alcohol.” Yes my identical twin boys Jamie and Eddie are two today! They’re off to Peppa Pig World to celebrate. I genuinely think I have the better deal by being in the city today.

August 2019 continues to throw up lots of interesting themes for those in the city with yesterday seeing the first ever print below 1% for Italian 10yr government bonds and a step towards a constitutional crisis here in the UK as PM Boris Johnson announced plans to effectively prorogue parliament from September 10th to October 14th when the government will hold a Queen’s Speech. As DB’s Oli Harvey noted in his report yesterday, this limits the ability of MPs to table legislation to prevent a no deal Brexit and signals that the Johnson government may be prepared to break constitutional precedent to take the UK out of the EU without a deal. However, Oli also highlights that at the same time, it could crystallise opposition to a no deal Brexit next week in the House of Commons leading to a confidence vote and a new unity government.

The reality now is that under the new schedule, UK parliament has just under a week in early September followed by just over a week in late October to prevent a no deal outcome. Assuming the timings are too tight and therefore legislation to block a no deal Brexit fails, the only option left for MPs would be a motion of no confidence in the government – either next week or in the last two weeks of October. Oli notes that much will now depend on the strategy taken by anti no deal MPs over the next two weeks. Our house view is still 50/50 for a no deal Brexit with the most likely path to preventing one being the formation of a national unity government either in early September or late October. There’s much more on the move in Oli’s note here including further scenario probabilities. My take on this is that it is partly a political move aimed at shoring up the support of leavers in the country and removing the need for such minded voters to support the Brexit Party at a General Election. The gamble is that the remain vote (probably also solidified the other way by this decision) would be more split across other parties (especially Labour and the Liberal Democrats). The more Parliament tries to blocks the move the more it could shore up support for Boris Johnson amongst the “leave” vote ahead of what might be a General Election before year-end. A fascinating and turbulent two months awaits us here in the UK.

In terms of markets the initial impact on Sterling was a drop of -1.08% from the highs to hit an intraday low of $1.216. However it did recover through the afternoon to end just -0.63% lower at $1.221 – not far off where it is in Asia this morning.

From a constitutional crisis to a political crisis which is at least showing signs of coming to a more peaceful end for now. In Italy it was another good day for Italian bonds as the PD confirmed that they support the current attempt to form a new government with Conte as premier. While the details over the exact coalition makeup is uncertain, President Mattarella did give Conte a fresh mandate to form a government last night. Markets took the news as broadly positive, with 10y BTPs at one stage dipping below 1% for the first time ever, before ultimately closing at 1.045% and -9.4bps on the day. A relentless move lower for bonds in Europe also saw Bunds close -2.0bps lower at -0.714% (a new all-time record after 8 days without one!) meaning the BTP-Bund spread is now at 176bps. At the end of May that spread was as much as 287bps so it’s been a remarkable rally. Elsewhere, Gilts closed -6.0bps lower at 0.442% as they tracked the move for Sterling. Across the pond Treasury yields edged lower again for much of the day but eventually moved higher on comments from the US Treasury Secretary Steven Mnuchin that issuing ultra-long debt is “under very serious consideration”. Yields on 10yr USTs (+0.8bps) ended at 1.481% while 30yr yields which were at one time trading at a fresh all-time low of just 1.942%, moved up +2.1bps to end the day at 1.972%. Meanwhile the 2s10s curve did steepen on Mnuchin’s comments to -2.2bps. However Treasury yields are again falling this morning with 10yrs down (-2.6bps) to 1.455% and just 9.7bps from all-time lows while the 30yr yield is down -4.5bps to an all-time low of 1.927%. The 2s10s curve has reversed much of the late steepening yesterday and is back down to -4.0bps this morning. Elsewhere oil rallied +1.82% yesterday after US inventories showed a -10mn barrel drawdown in crude stockpiles last week, which did appear to cap some of the move for bonds in the afternoon.

Overnight we’ve seen some fresh trade headlines which have highlighted the continued uncertain nature of the US-China trade talks. Firstly, the US Treasury Secretary Steven Mnuchin said that the US trade officials expect Chinese negotiators to visit Washington, but declined to say whether the September encounter would happen. He also added that “we will have a separate dialog and discussion on currency as part of the trade discussion but separate from the trade discussion,” and said, “we’ve had conversations with the IMF and directly with our counterparts in China, including the governor of the PBOC,” since the U.S. formally labeled China a currency manipulator on August 5. Separately, the White House trade adviser Peter Navarro said in an interview that market optimism on a US trade deal with China is neither misplaced nor well placed but “somewhere in the middle,” while adding that it’s “unlikely anything quick will happen,” from the talks because the U.S. is asking China to make big, structural changes. He also commented on the Fed, saying the Fed needs “to do its job and cut rates” in the next month or two. Elsewhere, Mnuchin said that the Trump administration doesn’t intend to intervene in the dollar market right now but added, “situations could change in the future but right now we are not contemplating an intervention.”

This morning in Asia markets are trading down with the Nikkei (-0.23%), Hang Seng (-0.36%), Shanghai Comp (-0.12%) and Kospi (-0.24%) all lower. In FX, the Japanese yen is trading up +0.189% this morning while the onshore Chinese yuan is trading flattish at 7.1667. Elsewhere, futures on the S&P 500 are down -0.33% while spot gold prices are up +0.33% to 1,544/ troy ounce.

We’ve also heard from the BoJ board member Hitoshi Suzuki overnight with him casting doubt on the stimulative effects of record-low Japanese government bond yields, while emphasizing the importance of monitoring their impact on financial stability. He further said that bank lending could also be hurt if rates are too low and added, “I think there’s a need to consider monetary policy more cautiously than we have so far.” 10yr JGBs yield are down -0.8bps this morning at -0.291% and just -0.4bps away from the September 2016 low of -0.295%.

Back to yesterday and equity markets were a bit more choppy as they sat in the shadows of the bond rally. Despite opening lower, the S&P 500 (+0.66%) ultimately finished higher. The energy sector (+1.40%) led gains, while other cyclical sectors gained as well. However the NASDAQ (+0.38%) and FANGs (+0.11%) indexes underperformed as tech struggled once more. On that, the Nikkei reported that Google was moving production of its Pixel smartphone out of China to Vietnam and plans to eventually move production of its US-bound hardware outside of China. Shares in Google closed +0.25% higher. As for trade headlines, there wasn’t much to report. Xinhau reported that China will start accepting waivers of additional tariffs between September 2 and October 18 which is perhaps a sign of flexibility from China and therefore slightly risk positive. From the US side, President Trump did tell reporters that he could do a deal, which would make him a “hero,” which was also, at the margin, a positive signal.

As for the data yesterday, there was very little to report. In Germany consumer confidence was unchanged in September at 9.7 while the July import price index reading was down a little more than expected at -0.2% mom. Meanwhile, the M3 money supply reading for the Euro Area was up +5.2% yoy, exceeding estimates for +4.7% and up from +4.5% in June. The only notable release in the US was the MBA mortgage index, which fell -6.3% last week. Given the recent collapse in rates, it’s somewhat worrying that mortgage activity hasn’t responded in a positive way.

On the Fed front, Richmond President Barkin spoke and gave a mostly balanced representation of the US economy. He said that “the US consumer appears to be very strong but business confidence appears to have weakened.” He explicitly said that he doesn’t know if he would support a rate cut in September, though in truth his opinion is not that important since he is not a voter. Fed fund futures continue to price in a near-certain rate cut next month, plus around a 12% chance for a larger, 50bps cut instead. We also heard from Kaplan and Daly overnight with both reinforcing last week’s message from central bank Chairman Jerome Powell that a September rate reduction is likely. Kaplan said, while consumer spending has been “strong,’’ the central bank needs to be “forward-looking’’ in setting interest rates and voiced concern that continued weakness in manufacturing would eventually seep into the jobs market, undermining consumer outlays. On dramatic decline in bond yields, Kaplan called it a “reality check” and attributed the decline in yields partly to global liquidity but added, “part of it is expectations of future growth have gotten a lot more pessimistic.”

Looking at the day ahead, this morning we’re due to get the final Q2 GDP revisions in France before August unemployment data is released in Germany and August confidence indicators due out for the Euro Area. This afternoon we’ll then get the August preliminary CPI release in Germany before all eyes turn to the second revision of Q2 GDP in the US. A reminder that the preliminary estimate showed growth of a stronger than expected +2.1%, with the consensus expecting a small roundown to +2.0% today. Also due out is the July advance goods trade balance, July wholesale inventories, latest jobless claims data and July pending home sales.

![]() Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/JvhhNtHqsE0/global-markets-soar-after-china-hints-trade-talk-optimism

Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/JvhhNtHqsE0/global-markets-soar-after-china-hints-trade-talk-optimism