Hedge Funds Have Never Been More Levered Or More Invested In The Same Handful Of Stocks

Hedge Funds Have Never Been More Levered Or More Invested In The Same Handful Of Stocks

Authored by Christopher Metli, Executive Director of MOrgan Stanley Quant Derivative Strategies

Investors largely shrugged off the factor rotation on Feb 4th as an isolated event, but it shouldn’t be dismissed – higher factor volatility is structural and is here to stay. Funds are taking bigger factor bets, positioning is crowded, leverage is high, and factor correlations are getting more unstable – all of which mean that future rotations will occur again (probably soon), and will likely be violent. While fully acknowledging that Fed liquidity is supportive of Growth stocks, it’s also true that the consensus believes the rally in Growth will continue. As a result QDS thinks the bar is low for an unwind should the economy change in either direction – a growth scare is the worst outcome for most investors, but growth acceleration can be painful too.

In this environment investors should consider:

- Replacing longs with upside calls in names that have rallied where volatility is low (i.e. stock replace, keeping upside but limiting downside)

- Hedging against sharp moves lower in the most vulnerable areas of the market – Crowded stocks (MSXXCRWD) or Growth vs Value (MSZZGRVL)

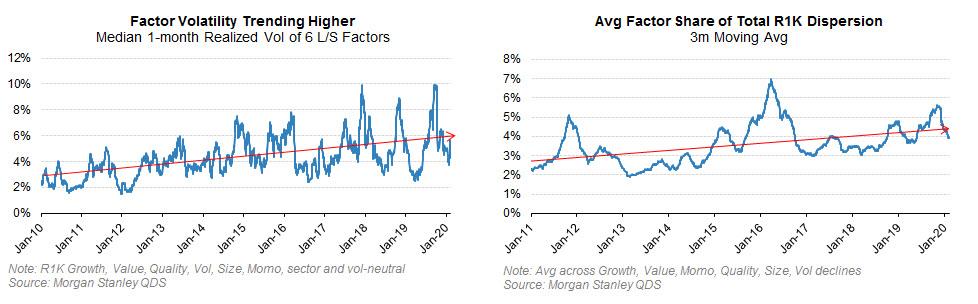

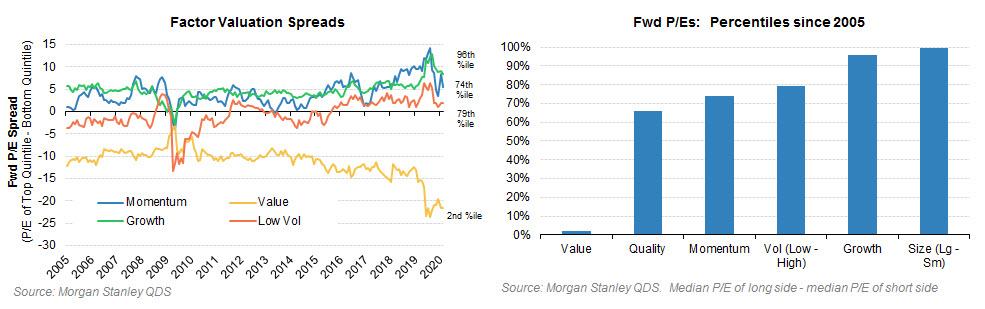

First, investors should recognize that the sources of risk have been shifting over the last 10 years. Factor volatility has been on a steady upward path since 2010. This impacts everyone (not just quants) because how stocks rank on factor scores now account for an increased portion of the total dispersion in the market.

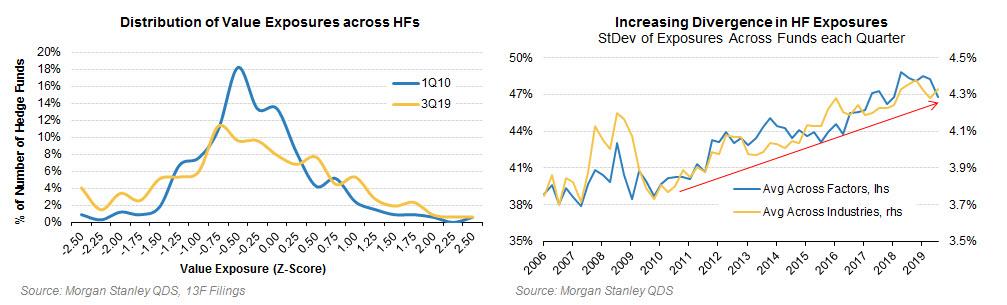

This increase in factor volatility is not a one-off event, it is a byproduct of HFs making bigger sector and factor bets than they were a few years ago. As one example, the chart below shows the distribution of Value exposures for discretionary long/short hedge funds in 2010 and in 2019, per public 13F filings. In 2010 HFs leaned short Value, just as they do now, but the distributions were much more tightly clustered around the mean. Today there are more funds in the tails running big overweights and big underweights. This trend is not limited to just Value or even factors – the distribution of overweights / underweights across sectors is also wider than it used to be.

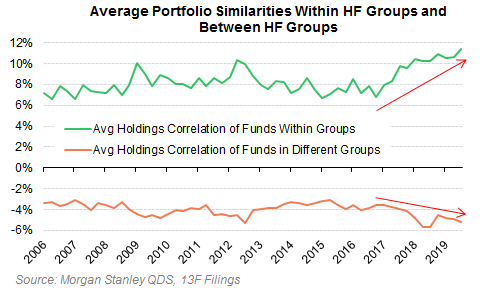

At the same time that factor and sector bets are getting bigger, funds making those bets are doing so in increasingly similar ways. QDS has found that within groups of hedge funds with similar styles, investor portfolios are getting more similar to each other. Similar portfolios means an increased risk of funds trading the same stocks at the same time.

Looking more recently, there is a concerning shift in the relative volatilities of factors. For all of 2019, Growth names became steadily less volatile than Value names – but this is now showing signs of reversal. Any increase in volatility in Growth is concerning because there is a greater overlap with the long side of investor portfolios (while Value is more representative of the shorts), and higher volatility on the long side of books is more dangerous because it impacts a broader investor base (note the Oct/Nov 2018 unwind had higher Growth volatility).

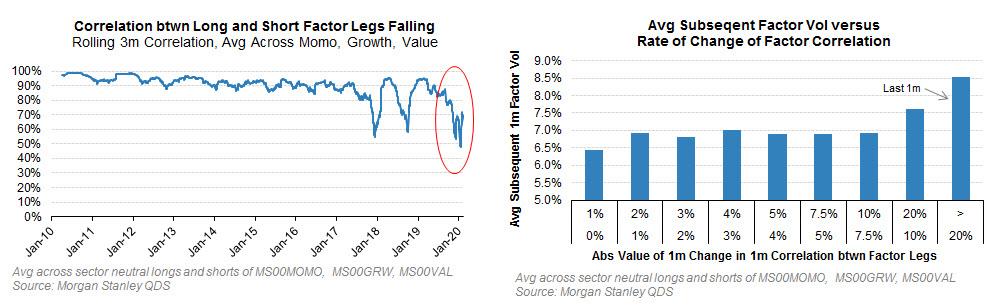

Another concerning dynamic is a recent breakdown in the correlation between the legs of different factors – i.e. the correlation between the long side of Momentum and the short side (and similar for Growth and Value) all fell in late 2019 into January 2020. Previous big declines in correlation were December 2017 and September 2018 – notably before big market volatility events. An increase in correlation instability like we are seeing now makes it harder for market participants to manage portfolios – and an increase in the rate of change of these correlations typically precedes higher factor volatility.

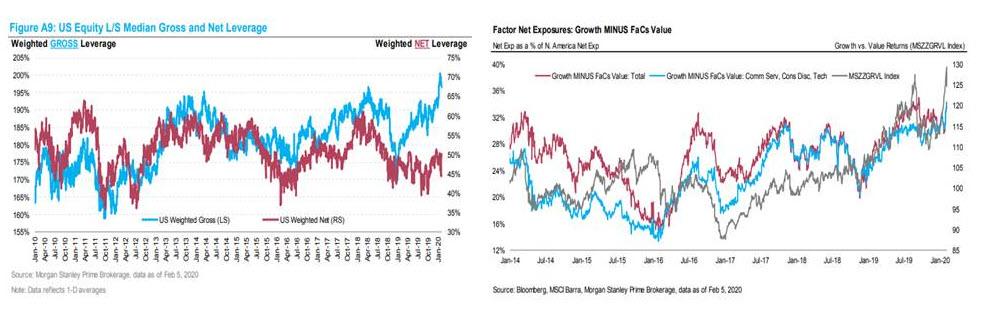

And then of course there is positioning. The MS PB Content team has noted that gross leverage for L/S hedge funds is near historical highs, while positioning in some (but not all) factors is extreme – Growth versus Value looks particularly stretched.

The MS PB Content team put out an excellent note in November titled ‘O Factors, Why Art Thou So Volatile?’ which addresses a lot of these topics. They find that higher gross leverage, a high level of crowding in the same stocks, and increased factor tilts has coincided with the increase in factor volatility over the last few years. And importantly they find that it has tended to be L/S discretionary hedge funds, not quants, whose flows have most correlated to factor volatility in the last few years. Contact your MS PB salesperson for the full report.

Trading Implications

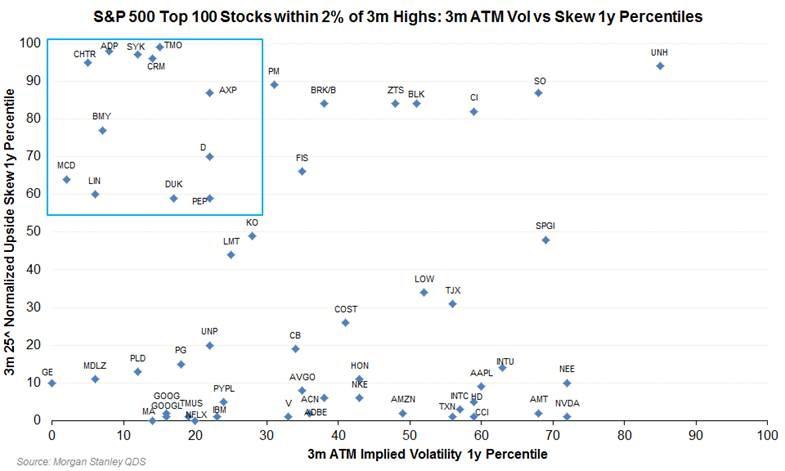

Fundamental traders with concentrated portfolios should consider replacing stretched longs with call options, retaining the upside but minimizing downside risks. The below screen shows top 100 S&P 500 stocks that are within 2% of recent highs – the upper left is where volatility is low and upside skew is steep. For example names like ADP, CRM, and CHTR in the highlighted box below have call options that price relatively attractively versus history.

Investors should also consider hedging some of the factor/crowding risks in their portfolios. In an unwind factor and thematic baskets can see an increase in correlation that means more downside making them good portfolio hedges. QDS’s preferred methods are:

- Short Growth versus Value (MSZZGRVL) given positioning for this factor remains stretched

- Short the most Crowded stocks (MSXXCRWD) versus going long the market or long Technology against it (for less net sector exposure)

Timing future unwinds is of course difficult, but given the instabilities in the market highlighted above QDS thinks it makes sense to trim some factor risk in portfolios.

Tyler Durden

Sun, 02/16/2020 – 11:35![]() Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/KeZ8jRdvhAI/hedge-funds-have-never-been-more-levered-or-more-invested-same-handful-stocks

Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/KeZ8jRdvhAI/hedge-funds-have-never-been-more-levered-or-more-invested-same-handful-stocks