In Ominous Warning, Ray Dalio Says The Current Period Is Just Like 1935-1945

Something has dramatically changed in the establishment’s view of central banking… and of the future.

As we reported earlier this week, recently we have observed a surprising spike in criticism of central banks by establishment figures, in some cases central bankers themselves, most notably Mark Carney who last Friday remarkably admitted that very low interest rates tend “to coincide with high risk events such as wars, financial crises, and breaks in the monetary regime” when he also urged an end to the dollar’s status as world reserve currency. This continued when 7 months after it praised negative rates, the San Francisco Fed pulled a U-turn and warned that the “Japanese experience”, where negative rates dragged down inflation expectations even more, is ground for NIRP caution.

There has never been so much hostility against central banks – even among other central bankers – in the past decade as over the past month. Something is about to snap

— zerohedge (@zerohedge) August 26, 2019

Meanwhile, as the FT concluded in its summary of last week’s Wyoming outing, “there was a sense that things will never be the same again” and quoted St Louis Fed President James Bullard, who wrote that “the developed world had experienced a “regime shift” in economic conditions: “Something is going on, and that’s causing I think a total rethink of central banking and all our cherished notions about what we think we’re doing,” Bullard admitted. “We just have to stop thinking that next year things are going to be normal.”

Tying it all together was Bank of America, which in anreport meant to recommend buying gold, lashed out at the Fed, warning that “ultra-easy monetary policies have led to distortions across various asset classes”; worse – and these are not our words, but of Bank of America – “it also stopped normal economic adjustment/renewal mechanisms by for instance sustaining economic participants that would normally have gone out of business”, i.e. a record number of zombie corporations. In addition, as everyone knows, debt levels have continued to increase, making it more difficult for central banks to normalize monetary policy as 2018 showed so vividly (and for Powell, painfully). Which brought us to BofA’s conclusion:

“We fear that this dynamic could ultimately lead to “quantitative failure”, under which markets refocus on those elevated liabilities and the lack of global growth, which would in all likelihood lead to a material increase in volatility.”

BofA wasn’t finished, however, and one day later, Bank of America doubled down when the bank’s FX strategist Athanasios Vamvakidis unleashing even more unexpected truth, and in a note justifying why further monetary easing is not the proper response to what ails the world now, writes that “the risks that monetary policy is trying to address are primarily the result of policy failures in other areas, which more central bank easing is unlikely to offset” and concludes that “we see increasing evidence that monetary policy easing in this environment supports asset prices more than the real economy. This increases risks for asset prices bubbles, with the eventual adjustment leading to a worse economy-the Greenspan mistake.“

* * *

All of which brings us to Wednesday’s highlight which was the latest scathing essay published by Bridgewater’s billionaire Chairman, Ray Dalio, titled “The Three Big Issues and the 1930s Analogue” in which he joins the pile up of Fed criticism, and echoes what BofA said, warning that central banks’ ability to reverse an economic downturn is coming to an end as the global economy enters what he says are the late stages of the long-term debt cycle.

The outcome could be nothing short of a global conflict (just as Carney hinted last Friday)

Specifically, the formerly optimistic Dalio (who can forget his lovely if fatally flawed “beautiful deleveraging” thesis) has turned downright Zerohedgish, and writes that the most important forces that exist now are:

- The End of the Long-Term Debt Cycle (When Central Banks Are No Longer Effective)

- The Large Wealth Gap and Political Polarity

- A Rising Work Power Challenging an Existing World Power

All of these combined to explain “The Bond Blow-Off, Rising Gold Prices, and the Late 1930s Analogue.”

In other words now 1) central banks have limited ability to stimulate, 2) there is large wealth and political polarity and 3) there is a conflict between China as a rising power and the U.S. as an existing world power.

While Dalio does not explicitly repeat Carney’s warning that extended periods of low rates lead to financial crisis and war, he does get to the same place in a circular fashion, saying that “if/when there is an economic downturn, that will produce serious problems in ways that are analogous to the ways that the confluence of those three influences produced serious problems in the late 1930s.“

We hope that everyone is familiar with what those “serious problems” were.

And actually, it is not true that Dalio does not reference the pernicious effects of low interest rates. After going through a brief recap of his economic outlook on the world, which he has summarized best in his video “How the Economic Machine works“, Dalio writes that “the most important things that are happening (which last happened in the late 1930s) are

- a) we are approaching the ends of both the short-term and long-term debt cycles in the world’s three major reserve currencies, while

- b) the debt and non-debt obligations (e.g., healthcare and pensions) that are coming at us are larger than the incomes that are required to fund them,

- c) large wealth and political gaps are producing political conflicts within countries that are characterized by larger and more extreme levels of internal conflicts between the rich and the poor and between capitalists and socialists,

- d) external politics is driven by the rising of an emerging power (China) to challenge the existing world power (the U.S.), which is leading to a more extreme external conflict and will eventually lead to a change in the world order, and

- e) the excess expected returns of bonds is compressing relative to the returns on the cash rates central banks are providing.

Is monetary policy able to counteract any of the above considerations? According to Dalio, the answer is no, as “we are classically in the late stages of the long term debt cycle when central banks’ power to ease in order to reverse an economic downturn is coming to an end because“:

- Monetary Policy 1 (i.e., the ability to lower interest rates) doesn’t work effectively because interest rates get so low that lowering them enough to stimulate growth doesn’t work well,

- Monetary Policy 2 (i.e., printing money and buying financial assets) doesn’t work well because that doesn’t produce adequate credit in the real economy (as distinct from credit growth to leverage up investment assets), so there is “pushing on a string.” That creates the need for…

- Monetary Policy 3 (large budget deficits and monetizing of them) which is problematic especially in this highly politicized and undisciplined environment.

This is also analogous to Carney’s warning that extended periods of low rates effectively become self-reinforcing and lead to catastrophic results.

And yet, central banks can’t just throw in the towel, so what are they to do? According to the Bridgewater billionaire, “central bank policies will push short-term and long-term real and nominal interest rates very low and print money to buy financial assets because they will need to set short-term interest rates as low as possible due to the large debt and other obligations (e.g. pensions and healthcare obligation) that are coming due and because of weakness in the economy and low inflation. Their hope will be that doing so will drive the expected returns of cash below the expected returns of bonds, but that won’t work well because…”

- a) these rates are too close to their floors,

- b) there is a weakening in growth and inflation expectations which is also lowering the expected returns of equities,

- c) real rates need to go very low because of the large debt and other obligations coming due, and

- d) the purchases of financial assets by central banks stays in the hands of investors rather than trickles down to most of the economy (which worsens the wealth gap and the populist political responses).

Compounding the complexity, this is happening at a time when investors “have become increasingly leveraged long due to the low interest rates and their increased liquidity. As a result we see the market driving down short term rates while central banks are also turning more toward long-term interest rate and yield curve controls, just as they did from the late 1930s through most of the 1940s.”

Then just as importantly Dalio says that the current period is a mirror image “symmetrical reversal” of the inflationary explosion of the late 1970s/early 1980s, a period he calls a “dis/deflationary blow-off”, and urges readers to “look at the current inflation rates at the current cyclical peaks (i.e. not much inflation despite the world economy and financial markets being near a peak and despite all the central banks’ money printing) and imagine what they will be at the next cyclical lows. That is because there are strong deflationary forces at work as productive capacity has increased greatly.”

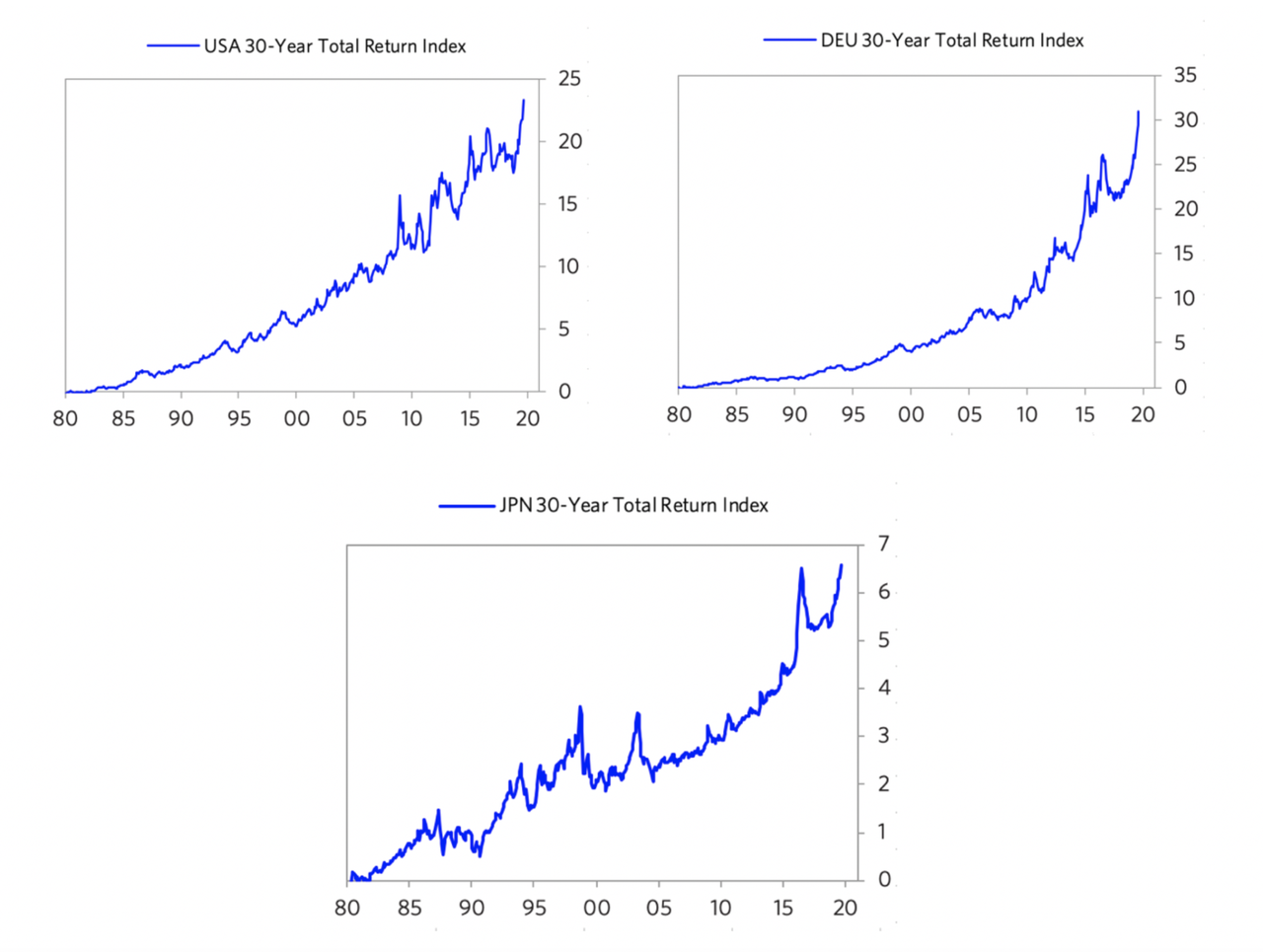

It is these deflationary forces – including debt, demographics and technology – that are creating “the need for extremely loose monetary policies that are forcing central banks to drive interest rates to such low levels and will lead to enormous deficits that are monetized, which is creating the blow-off in bonds that is the reciprocal of the 1980-82 blow-off in gold.” The charts below show the 30-year T-bond returns from that 1980-82 period until now, which highlight the blow-off in bonds.

Which brings us to Dalio’s conclusion, which finds that the epic build up of imbalances in the economy can be traces to one specific period in history: that of World War II:

To understand the current period, I recommend that you understand the workings of the 1935-45 period closely, which is the last time similar forces were at work to produce a similar dynamic.

If that sounds surprisingly familiar to what Mark Carney said last Friday, when he warned that low rates lead to “crisis and war”, it is probably not a coincidence. Of course, not looking to be blamed for catalyzing the next world war, Dalio caveats that he is “not saying that the past is prologue in an identical way. What I am saying that the basic cause/effect relationships are analogous:

- a) approaching the ends of the short-term and long-term debt cycles, while

- b) the internal politics is driven by large wealth and political gaps, which are producing large internal conflicts between the rich and the poor and between capitalists and socialists, and

- c) the external political conflict that is driven by the rising of an emerging power to challenge the existing world power, leading to significant external conflict that eventually leads to a change in the world order.

As a result, Dalio concludes, “there is a lot to be learned by understanding the mechanics of what happened then (and in other analogous times before then) in order to understand the mechanics of what is happening now. It is also worth understanding how paradigm shifts work and how to diversify well to protect oneself against them.”

Considering that the period Dalio says is most comparable to the current “paradigm shift” culminated with world war that resulted in the deaths of tens of millions, we are very curious what Dalio would recommended to “protect oneself” from what is coming. Or is a “beautiful world war” just the inevitable next step when “beautiful deleveraging” fails?

![]() Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/rDPMWiFaWaM/ominous-warning-dalio-says-current-period-just-1935-1945

Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/rDPMWiFaWaM/ominous-warning-dalio-says-current-period-just-1935-1945