Markets Hit By “Perfect Storm” As Stocks Slide On Surge In New Coronavirus Cases, Deaths

Markets Hit By “Perfect Storm” As Stocks Slide On Surge In New Coronavirus Cases, Deaths

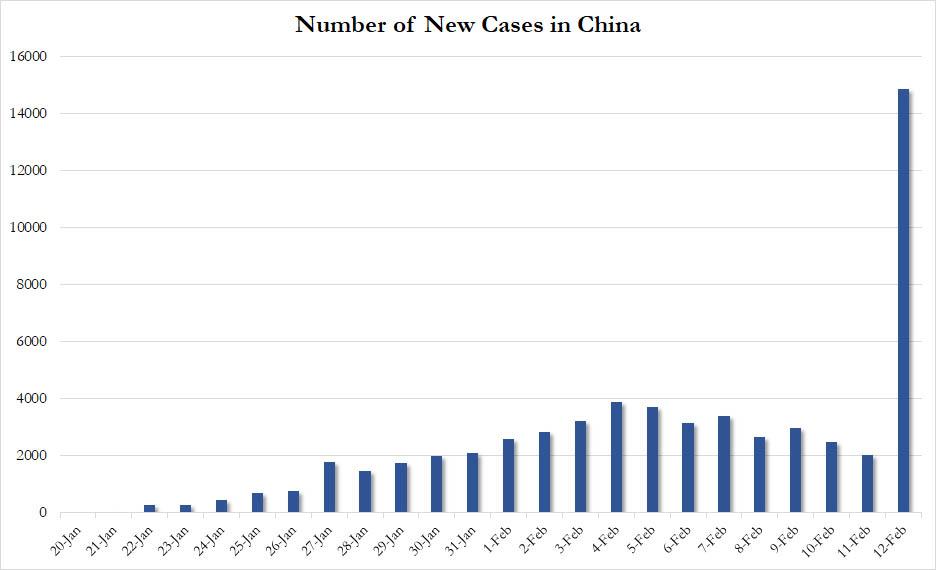

For weeks we had been warning that China was misrepresenting, obfuscating and otherwise lying, either directly or simply by changing the definition of an “infected case” or even “death”, about the true extent of the corona pandemic, a conclusion that was obvious by simply looking (here and here) at the underlying “official” data. This morning, the quants and algos got a huge shock when China was finally overwhelmed with the level of lies – and cremated bodies – since the breakout of the covid pandemic, and was forced to “adjust” the number of new cases higher by a whopping 15,000. Think of it as GAAP virus accounting vs non-GAAP, which excludes the inconvenient “one-time” cases.

The result has been a sharp drop in US equity futures and global stock prices, as it raised fresh questions about the scale of the crisis and more importantly, how long it will take China to truly contain the pandemic, even as markets had taken comfort from the World Health Organization’s emergency program head describing the apparent slowdown in the epidemic’s spread as “very reassuring”. Oops.

As a reminder, with consensus expecting China to regain control in the next few weeks, any delay puts the V-shaped Q2 China (and global) GDP recovery in peril, and as such the longer China pushes back on this critical D-day, the harder it will be for traders to pretend the pandemic is not happening.

The sharp rise in the headline number of deaths and infections unnerved world markets, as traders halted a recent rally in stocks and retreated back to the safety of government bonds and gold.

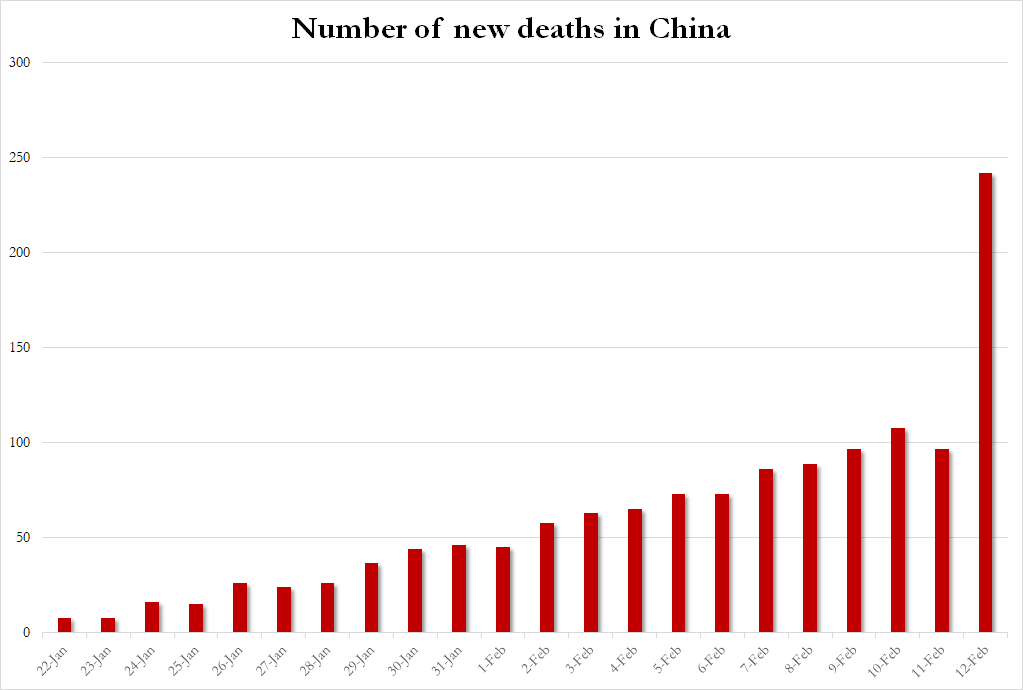

It wasn’t just the surge in new cases: health officials in China’s central province of Hubei – at least those who weren’t summarily fired in the past few days – said 242 people had died from the flu-like virus on Wednesday, the fastest rise in the daily count since the pathogen was identified in December. Apparently this too was due to a change in definition as until now China was representing coronavirus deaths as the result of something far more innocent such a pneumonia. Well no more.

The new deaths took the total to 1369 vs. 6,017 recovered. That’s an 18.5% fatality rate if one looks at that ratio, and a ‘Spanish Flu’ 2.2% if one looks at total cases, if they are now accurate, according to Rabobank.

Ironically, the surge in numbers came a day after markets cheered when China reported its lowest number of new cases in two weeks, bolstering a forecast by the country’s senior medical adviser that the epidemic could end by April. Well, no more.

“Just when markets were getting comfortable with the idea that the Covid-19 infection increase was trending lower, the sudden jump in the number of new cases in Hubei has jolted them out of this sense of complacency,” said Khoon Goh, head of Asia research at Australia & New Zealand Banking Group Ltd.

Hubei had previously only allowed infections to be confirmed by RNA tests, which were limited to roughly 3,000 per day (as we also noted) and can take days to process. But as it was overwhelmed by new cases, it was forced to start using quicker computerized tomography (CT) scans, which reveal lung infections, usually manifesting themselves only in very advanced, of not outright terminal, cases, the Hubei health commission said, to confirm virus cases and isolate them faster. As a result, another new 14,840 cases were reported in the central province on Thursday, from 2,015 new cases nationwide a day earlier. The new diagnostic procedure could explain the spike in deaths, said Raina McIntyre, head of biosecurity research at the Kirby Institute at the University of New South Wales. “Presumably, there are deaths which occurred in people who did not have a lab diagnosis but did have a CT,” she told Reuters. “It is important that these also be counted.”

The new methodology effectively lowers the bar for classifying new infections, contributing to the spike in cases. Chinese officials said the method is only being used in Hubei, though it was expected to be gradually extended to other regions.

In total, about 60,000 people have now been confirmed to have the virus, the vast majority of them in China, although it is very possible that there will be far more global cases once those infected start manifesting symptoms.

And as the full extent of the pandemic slowly emerges, trader optimism and “hopes” were finally sapped, and European markets – trading at all time highs on Tuesday – quickly followed Asia into red with London FTSE, Frankfurt’s DAX and Paris’ CAC 40 down 0.3% to 0.9%, and the euro slumped near a three-year low against the dollar after a torrid couple of weeks.

AXA Investment Management’s chief economist Gilles Moec said the impact of virus could be part of a “perfect storm” for Europe that hurts the economy for months and then gets compounded by a heated trade battle with the United States.

“We started with the premise that this virus would be worse that SARS and that has become consensus,” Moec said. “So attention turns to who is hit the hardest and Europe is among the usual suspects and Germany in particular give China is its biggest export market. So the reaction of the exchange rate is probably rational,” he added.

E-mini S&P 500 futures were also down 0.5%, pointing to a fade in Wall Street’s strong rally.

With investors seeking safety, 10-year U.S. Treasuries fell below 1.6% European yields fell around 3 basis points, the yen strengthened past 110 per dollar and a rally in oil prices halted.

The Stoxx Europe 600 Index was on pace for its biggest drop this month, dragged lower by miners and banks. Barclays slipped as the bank revealed British regulators are probing Chief Executive Officer Jes Staley’s relationship with financier Jeffrey Epstein. Alibaba Group Holding Ltd. edged up in the pre-market after quarterly revenue rose more than expected.

MSCI’s broadest index of Asia-Pacific shares outside Japan had snapped two days of 1% gains to end 0.1% lower as most markets across the region posted modest declines. Japan’s Nikkei fell 0.1%. Australia’s ASX/S&P 200 index retreated from a record high. The Shanghai Composite fell 0.6% and Hong Kong’s Hang Seng was 0.3% softer. Gold rose 0.6% to $1574 per ounce. Overall, Asian stocks swung between gains and losses, as advances in technology stocks were offset by declines in financial and industrial shares. The MSCI Asia Pacific Index was little changed as markets in the region were mixed. Australia’s S&P/ASX 200 gained, while regional gauges for China and Hong Kong snapped a recent rebound.

“There is no panic on this,” said Frank Benzimra, head of Asia equity strategy at Societe Generale in Hong Kong, since the dramatic rise seems so far to be contained to Hubei.

Maybe there is “no panic” but even Benzimra himself logged in from home and speaking to clients by phone as meetings are increasingly canceled, even in cities not subject to quarantine. “Most markets were recouping their losses so that has offered maybe some excuse to sell Asian markets,” he said. “But there is not much energy in this.”

What happens next? Morgan Stanley believes a gradual, rather than sharp recovery is the most likely scenario, and the longer it takes China to contain the pandemic, the more delayed the recovery will be. That all bodes ill for regional economies and has weighed on Asian currencies and commodities.

In FX, the yen rallied and the Swiss franc advanced to its strongest level since 2015. Japan’s currency gained versus all major peers and German bunds followed Treasuries higher. The Swiss franc touched 1.0622 per euro, its strongest level since August 2015, as the shared currency was weighed down by speculation of further ECB easing and concerns about Germany’s political stability. The Bloomberg Dollar Spot Index edged lower and the greenback traded mixed against Group- of-10 peers; the U.S. currency reversed Asia-session gains after after touching yesterday’s high of 1.0865 per euro. The euro’s slump to a nearly three-year low versus the dollar seems to have caught some investors off guard and options traders are responding to the risk that the move has further legs. The Australian dollar, a liquid proxy for China’s economic health because of Australia’s export exposure, retraced its recent rally and traded 0.3% softer at $0.6716. China’s yuan was 0.1% weaker, while the pound gained after Sajid Javid quit as the U.K.’s Chancellor of the Exchequer.

In commodities, rallying oil prices stalled, with Brent crude flat at$55.72 per barrel, 15% below where it was before the coronavirus outbreak.

To the day ahead now, the data highlight comes from the US today, where there’ll be the release of January’s CPI reading as well as weekly initial jobless. In terms of central bank developments, the Senate Banking Committee will be holding a hearing into the nomination of Judy Shelton and Christopher Waller to the Federal Reserve Board of Governors. Other speakers include the ECB’s Hernandez de Cos, Panetta and Lane, along with Kaplan and Williams from the Fed. There’ll also be a policy decision from the Banco de Mexico. Lastly, earnings highlights out today include Nissan, PepsiCo, AIG and Nvidia, and separately, the European Commission will be presenting their Winter 2020 economic forecasts.

Market Snapshot

- S&P 500 futures down 0.8% to 3,353.75

- STOXX Europe 600 down 0.6% to 428.76

- MXAP down 0.1% to 170.83

- MXAPJ down 0.08% to 556.11

- Nikkei down 0.1% to 23,827.73

- Topix down 0.3% to 1,713.08

- Hang Seng Index down 0.3% to 27,730.00

- Shanghai Composite down 0.7% to 2,906.07

- Sensex down 0.3% to 41,460.48

- Australia S&P/ASX 200 up 0.2% to 7,103.23

- Kospi down 0.2% to 2,232.96

- German 10Y yield fell 2.6 bps to -0.404%

- Euro up 0.1% to $1.0886

- Italian 10Y yield fell 5.4 bps to 0.748%

- Spanish 10Y yield fell 3.4 bps to 0.276%

- Brent futures down 1% to $55.22/bbl

- Gold spot up 0.6% to $1,575.23

- U.S. Dollar Index down 0.2% to 98.88

Top Overnight News from Bloomberg

- China took action on two fronts to gain control of the spiraling coronavirus outbreak: reporting a dramatic increase in cases and ousting top officials who failed to check the disease’s expansion; car sales in the country plunged to fresh lows in January as buyers stayed away from showrooms

- European economic malaise is set to continue this year, the bloc’s executive said, warning a deadly viral outbreak could further damp the outlook. The European Commission singled out the coronavirus as a “key downside risk”

- Boris Johnson fired a clutch of senior U.K. ministers including Business Secretary Andrea Leadsom — a former rival for the Conservative party leadership — in a dramatic cabinet cull on Thursday. After winning a majority in December’s election, the British prime minister is stamping his authority on his top team to bring in new blood and prepare the U.K. for life after Brexit

- Some investors are paying up to hedge against the risk that the Fed will need to cut interest rates much more deeply than most expect this year. Traders on Wednesday bought out-of-the-money December and March eurodollar call options with a strike price of 99.50, which stand to benefit if policy makers make around three or more cuts

- The ECB is looking for ways to favor environmentally friendly bonds in a fresh bid to intensify its fight against climate change. While buying environmentally friendly bonds for political reasons is a non-starter, officials are focusing instead on less controversial options. A key part of that is recognizing that purchasing carbon-intensive securities comes at a risk to the institution itself

- Italy is in danger of missing its already unambitious growth targets for 2020 because of the coronavirus outbreak, according to a senior government official

Asian equity markets traded cautiously as the euphoria from the record highs on Wall St were soured by a significant jump in the number of additional coronavirus cases. The Hubei province reported 14840 new coronavirus cases under revised standards and 242 more deaths as of February 12th in which 13332 of the cases were made by clinical diagnosis. Nonetheless, ASX 200 (+0.2%) remained afloat with a slew of earnings the main driver for the biggest movers in the index including Big 4 bank NAB and with TPG Telecom bolstered after the federal court approved its merger with Vodafone Hutchison Australia, while Nikkei 225 (-0.1%) succumbed to the flows into the JPY and as participants also digested quarterly results. Elsewhere, Hang Seng (-0.3%) and Shanghai Comp. (-0.7%) were subdued amid uncertainty following the surge in confirmed cases and although some suggested the number would have been less than the prior day without the adjustments, the number of new fatalities more than doubled. Finally, 10yr JGBs were choppy amid the cautious risk tone and after the BoJ’s presence in the market for over JPY 1.2tln of JGBs heavily concentrated in 1yr-10yr maturities, did little to spur demand for the benchmark.

Top Asian News

- China Navigates the Latest Threat to Its Debt-Fueled Boom

- MUFG Hong Kong Staff Told That Some Employees Under Quarantine

- Tencent’s $127 Billion Rally Bolstered by Work-From- Home Masses

- Malaysia Plans Stimulus as Virus May Worsen Growth at Decade Low

European stocks trade with losses across the board [Eurostoxx 50 -1.4%] following on from a similar APAC handover, as sentiment took a blow following an unprecedented rise in COVID-19 cases after an adjustment to standards. Bourses are firmly in the red, with the FTSE 100 (-1.7%) underperforming regional peers amid a slew of factors including losses in large-cap miners, oil giants and heavyweight financials. Market contacts highlighted notable selling program triggered for Eurostoxx 50 futures and a technical break below yesterday’s low in the DAX exacerbated downside. Sectors are largely lower but reflect risk aversion as defensive fare modestly better than cyclicals, with materials and energy sectors underperforming amid price action in their respective complexes. Back to the FTSE, Barclays (-2.0%) shares fell post-earnings after the Co. noted that it would be challenging to reach a 2020 ROTE of over 10%, while UK regulators opened a probe into CEO Staley’s link to Jeffrey Epstein. Meanwhile, miners bear the brunt of declines across the base metal markets – with Antofagasta (-1.7%), Glencore (-1.9%) and BHP (-0.8%) all lower. Similarly, oil giants feel downward pressure from the price action in the energy complex, albeit BP (-2.9%) and Shell (-3.0%) also trade ex-div today. Elsewhere, SMI-heavyweight Nestle (-2.3%) shares fell after missing revenue and organic sales growth forecasts whilst also halting the production of its low-sugar brand due to coronavirus’ impact. Note: Nestle has ~19% weighting in the SMI and ~3.2% weighing in the Stoxx600. Credit Suisse (-0.7%) shares fell with the broader market after initially seeing some reprieve from earnings after posting a 69% jump in annual net profit despite the spying scandal. Other earnings-related movers include Orange (+1.9%), Centrica (-16%), Zurich Insurance (+0.7%), Clariant (+4.9%) and Pernod Ricard (+1.7%)

Top European News

- Johnson Overhauls Cabinet for Life Outside EU: U.K.Reshuffle

- Barclays’ Staley Faces Probe on Transparency of Epstein Ties

- Thyssenkrupp Says Elevator Sale Is Imminent as Losses Mount

- Europe’s Recovery from Manufacturing Slump Hit by Coronavirus

In FX, the traditional safe-havens are back in demand and outperforming, as revised classification standards used to determine whether an individual has contracted the coronavirus at the source in Hubei has hugely inflated the number of confirmed cases and reignited concerns about the overall tally and contagion, especially if the new methodology is rolled out to other provinces. In response, the Yen is back above 110.00, the Franc is nearer 0.9750 than 0.9800 and Gold is back up around Usd 1575/oz from circa Usd 1560 at one stage yesterday, while the Dollar has pulled back accordingly.

- GBP/EUR – Sterling remains relatively resilient in the face of the downturn in broad risk sentiment, albeit partly due to the Greenback losing momentum, as noted above, and the Euro continuing to depreciate amidst weak fundamentals and more outflows against currencies that are costlier to fund. However, Cable is still capped ahead of 1.3000 and the 10 DMA (1.2984 today) that was matched, but not surpassed and Eur/Gbp has not spiralled down through 0.8400 as Eur/Usd holds just above key Fib support (1.0864), for now at least.

- USD – The DXY has slipped a bit further from Wednesday’s new multi-month high (99.052 to 98.852) on the aforementioned deterioration in risk appetite that has boosted the Jpy, Chf and Xau, though the index and Buck overall remains underpinned ahead of US CPI, weekly claims and more Fed speak via Williams. Technically, 99.249 forms nearest chart resistance, while support resides down at 98.544.

- CAD/NZD/AUD/NOK/SEK – The Loonie has lost its crude prop, but is gleaning enough support to hold around 1.3250 after comments from BoC Governor Poloz reiterating the cons of looser monetary policy and claiming that Canada’s economy is in a good place, while the Kiwi is consolidating off post-RBNZ peaks circa 0.6450 following Deputy Governor Hawkesby underlining a genuine neutral stance and the Aussie is acknowledging RBA Governor Lowe reiterating a wait-and-see bias given no rush to get inflation back to target as Aud/Usd meanders in the low 0.6700+ area and Aud/Nzd pivots 1.0425. Ahead, NZ manufacturing PMI and food prices. Elsewhere, the Norwegian Crown is naturally more attune to a dip in oil prices, but its Swedish peer is also wary about a return to risk aversion.

- EM – Widespread declines vs the Dollar including the Yuan for obvious reasons, but also the Lira even though Turkish ip beat consensus and the Rand regardless of a more pronounced recovery in SA mining production. Similary, the Mexican Peso is on the back foot awaiting the anticipated 25 bp Banxico rate cut later today.

- Bank of Canada Governor Poloz said the Canadian economy is in a pretty good place and suggested that lowering rates could increase risks from higher debt levels. (Newswires)

- RBA Governor Lowe said outlook in Australia is improving but added that coronavirus is having an uncertain impact and noted that Chinese policy stimulus will be good for Australia. Furthermore, RBA Governor Lowe said low interest rates are working and are going to take time, while he added they are not obsessed with getting inflation back to target in a hurry. (Newswires)

- RBNZ Assistant Governor Hawkesby said the RBNZ has a genuine neutral bias but is open to review that in light of developments, while he added that the impact from coronavirus expected to be modest but will review it if travel restrictions are prolonged or virus is more widespread. (Newswires)

In commodities, WTI and Brent front-month futures have erased a bulk of the prior session’s gains, with prices south of 51/bbl and 55.50/bbl respectively, as the unexpected jump in coronavirus cases sparked risked aversion, while no sense of urgency from Russia regarding output action also adds to the bearish narrative. Further on the OPEC front, Kremlin stated that Moscow has not yet decided on further action with OPEC on oil cuts, adding that it will announce a deal in due course – as a reminder, the Russian Energy Ministry met with domestic oil producers yesterday with some comments alluding to most Russian companies wanting the cuts to be continued for one more quarter. Elsewhere, the IEA monthly oil report downgraded its 2020 demand growth forecast by 365k BPD – the deepest among the three oil market reports, citing impacts of the coronavirus on demand. This follows OPEC and EIA slashing their respective 2020 global oil demand growth forecasts by 230k BPD and 310k BPD. Elsewhere, spot gold retains an underlying bid amid the risk-off sentiment with prices meandering 1575/oz. Conversely, copper sees sentiment-driven losses with prices back below 2.6/lb after briefly reclaiming the level

US Event Calendar

- 8:30am: US CPI MoM, est. 0.2%, prior 0.2%; CPI Ex Food and Energy MoM, est. 0.2%, prior 0.1%

- 8:30am: US CPI YoY, est. 2.4%, prior 2.3%; CPI Ex Food and Energy YoY, est. 2.2%, prior 2.3%

- 8:30am: Real Avg Hourly Earning YoY, prior 0.6%; Real Avg Weekly Earnings YoY, prior 0.0%

- 8:30am: Initial Jobless Claims, est. 210,000, prior 202,000; Continuing Claims, est. 1.73m, prior 1.75m

- 9:45am: Bloomberg Consumer Comfort, prior 66.5

Central Banks

- 10am: Senate Panel Holds Hearing for Fed Nominees Shelton, Waller

- 12:45pm: Fed’s Kaplan Speaks in Texas

- 5:30pm: Fed’s Williams Speaks in New York

DB’s Jim Reid concludes the overnight wrap

Although the survey suggests concerns over the virus and the growth impact hover in the background, markets have continued to take heart from increasing signs that the coronavirus’ impact on the global economy will be manageable; however, a jump in the number of cases in Hubei this morning following what appears to be a change in methodology in the way cases are diagnosed has seen markets stall in Asia. The number of reported cases in China’s Hubei province has jumped by 14,840 and fatalities by 242. Meanwhile, Japan has also confirmed another 44 cases on the quarantined ship, bringing the total of infections from the vessel to 218 while the US also confirmed another case overnight bringing the tally there to 14. Also as we go to print news wires are reporting that in Vietnam, local authorities have placed a commune of 10,600 people in isolation after at least 10 cases of the novel coronavirus were confirmed in Vinh Phuc province. Elsewhere, Hong Kong has extended the closure of schools until at least March 16 and United Airlines said that it will extend the suspension of China flights until April 24. At a more micro level, MGM Resorts International withdrew its earnings forecast for 2020, citing the unpredictable impact of the virus on its casinos in Macau and Las Vegas. See our China economist’s latest update on the impact of the virus here.

The main bourses in Asia are all down as a result, including the Nikkei (-0.27%), Hang Seng (-0.26%), Shanghai Comp (-0.67%) and Kospi (-0.03%), however the extent of the drops are fairly modest. Staying with Asia it’s worth noting that the Chinese Communist Party’s top decision body said overnight that the economic and social goals for 2020 will be met by keeping the prudent monetary policy flexible and appropriate, making greater use of fiscal policy, boosting domestic consumption, and promoting large foreign-investment projects.

Prior to the small risk-off this morning, US equities powered forward to new highs last night, with the S&P 500 advancing a further +0.65%, to put the index up +4.77% on a month-to-date basis now and marking the 3rd consecutive session that the index has hit a record high. The US index has traded up every day this week, and is now up in 7 of the last 8 trading sessions. Risk assets made gains across the board, with the NASDAQ (+0.90%) and Dow Jones (+0.94%) also at new records, along with the STOXX 600 (+0.63%) and the DAX (+0.89%) in Europe. Energy stocks outperformed, bolstered by oil’s strong performance, with both Brent crude (+3.30%) and WTI (+2.46%) up strongly, with Brent having its best day since early January. Meanwhile, investors moved into peripheral European debt, with Greek 10yr yields falling below 1% in trading for the first time ever, while the spread of BTPs over bunds fell -6.8bps, closing at their tightest level since May 2018. Meanwhile, the Euro (-0.38%) hit its lowest level against the Dollar since May 2017 – and down 7 out of the last 8 days – as concerns over the European economy linger. A fair amount of press has been given to DB’s piece earlier this week on the risks of a technical recession in Germany post the Coronavirus. See the report here ahead of Q4 GDP on Friday.

Having said that, and as discussed above, risk was in a bullish mood yesterday. Another factor that may have supported this were the results from New Hampshire that we reported this time yesterday. Although Bernie Sanders, came out on top, this was only with 25.7% of the vote, which was actually c.3 points below his polling in the RealClearPolitics average. Furthermore, as we discussed yesterday, if you add up support for the 3 more centrist candidates (Buttigieg, Klobuchar and Biden), they actually got a majority of the popular vote (52.6%), suggesting Mr. Sander’s arithmetic towards the nomination may still be tricky, especially with Mr Bloomberg set to imminently enter the race. Perhaps our survey respondents see this?

In terms of the latest on the race, we’ll have to wait until a week on Saturday for the next set of voting in Nevada. There are increasing questions being asked about the viability of former Vice President Joe Biden’s campaign, having come in 4th and 5th place, respectively, in the first 2 contests. He’s setting up South Carolina as his firewall later in the month, as his support is much stronger among African American voters, whereas both Iowa and New Hampshire are among the least racially diverse states in the US. That said, it’ll be an uphill struggle, and going back to 1972, the eventual Democratic presidential nominee has always come either first or second in New Hampshire, so it would certainly break that run were someone other than Mr. Sanders or Mr. Buttigieg manage to win. Furthermore, the last person to win the Democratic nomination without winning either of the first two states was Bill Clinton back in 1992.

Staying with the United States, Fed Chair Powell testified before the Senate Banking Committee yesterday, though there wasn’t a great deal that was newsworthy out of his remarks following his testimony the previous day before the House Financial Services Committee. When Mr. Powell was asked about the coronavirus, he said it was “too uncertain to even speculate”. In terms of other Fed speakers, we also heard from Philadelphia Fed President Harker, who’s a voting member on the FOMC this year. Regarding rates, he said that his “own view right now is that we should hold steady for a while and watch how developments and the data unfold before taking any more action.” 10yr Treasury yields closed up +3.3bps yesterday, with the 2s10s curve steepening by +1.2bps.

In terms of central banks elsewhere, the Riksbank left rates unchanged yesterday at 0%, in line with expectations, and left their forecast for the repo rate the same as in December. They did lower their inflation forecast, with the 2020 CPIF forecast downgraded to +1.3%, having been +1.7% back in December, though they also revised growth up a tenth for 2020, 2021 and 2022. On the data front, there wasn’t a great deal out yesterday, but the Euro Area industrial production numbers showed a -2.1% decline in December (vs. -2.0% expected), the biggest monthly contraction since February 2016.

To the day ahead now, and the data highlight comes from the US today, where there’ll be the release of January’s CPI reading as well as weekly initial jobless claims, while from Europe we’ll get the final reading of German CPI for January. In terms of central bank developments, the Senate Banking Committee will be holding a hearing into the nomination of Judy Shelton and Christopher Waller to the Federal Reserve Board of Governors. Other speakers include the ECB’s Hernandez de Cos, Panetta and Lane, along with Kaplan and Williams from the Fed. There’ll also be a policy decision from the Banco de Mexico. Lastly, earnings highlights out today include Nissan, PepsiCo, AIG and Nvidia, and separately, the European Commission will be presenting their Winter 2020 economic forecasts.

Tyler Durden

Thu, 02/13/2020 – 08:04![]() Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/2FU9i2PKgqU/markets-hit-perfect-storm-stocks-slide-surge-new-coronavirus-cases-deaths

Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/2FU9i2PKgqU/markets-hit-perfect-storm-stocks-slide-surge-new-coronavirus-cases-deaths