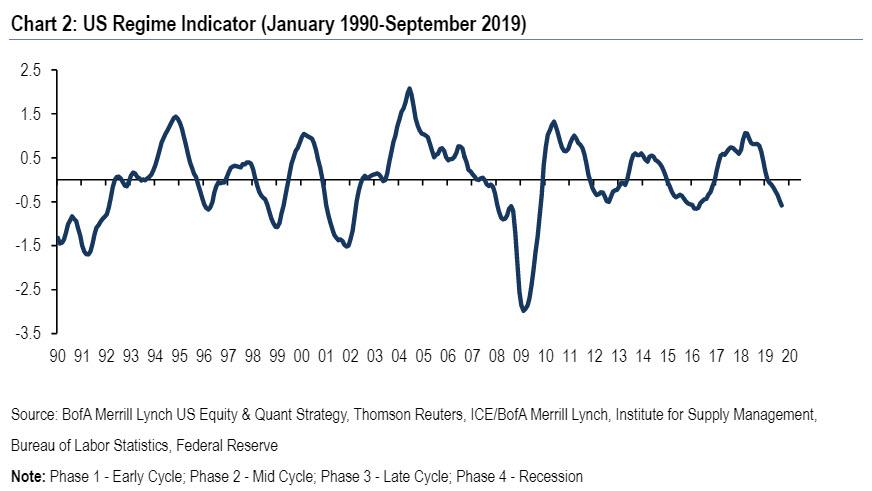

“Risk Of Imminent Whipsaws”: BofA’s Regime Indicator Is In The Last Month Of Its “Downturn” Phase

“Risk Of Imminent Whipsaws”: BofA’s Regime Indicator Is In The Last Month Of Its “Downturn” Phase

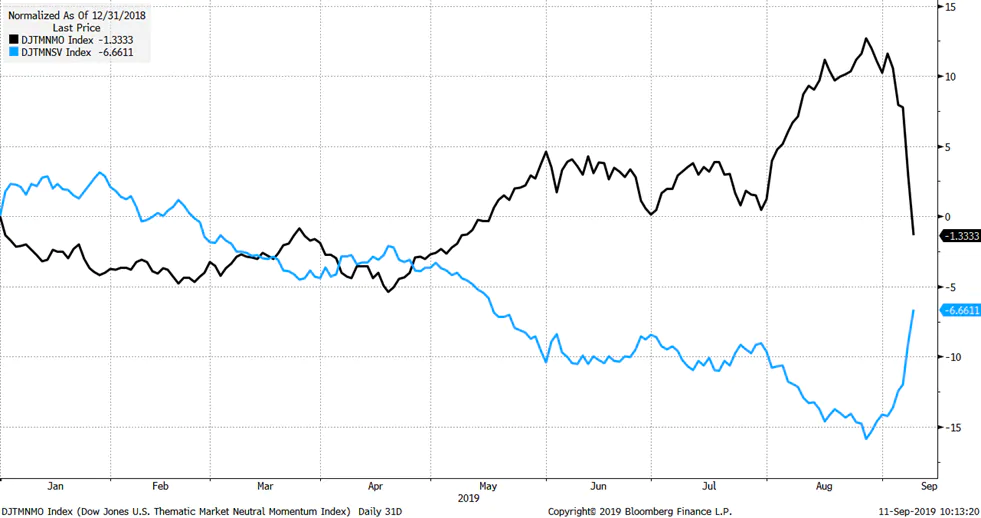

A little over a month after the early September quant quake, which sent momentum and growth stocks plunging and value stocks surging…

… things are largely bank to normal, with growth continuing its steady outperformance (despite the occasional puff piece to prevent value investors from jumping off tall buildings) as value stumbles.

However, according to a new report from BofA, what happened in September may merely be an appetizer of what is to come, as the outperformance by momentum/growth is finally be coming to an end according to the bank’s strategists. Warning that “whipsaw risk is elevated and imminent”, BofA’s Savita Subramanian writes that “value is neglected and cheap, momentum is crowded & expensive” while ultra-negative Momentum/Value correlations indicate undue stress.

In other words, “we are at the trickiest part of the cycle.” Here’s why.

According to BofA’s proprietary Regime Indicator, we are now in month seven of the “Downturn” phase, which on average, has lasted eight months. And, as the bank’s strategists argue, “the only way to exit this phase is by moving into “Early Cycle” (that, or something much worse).

The reason why this is important is that factors that do well during the “Downturn” phase (quality, large caps, low risk, anti-value) are the opposite to those that lead during “Early Cycle” (beta, small size, deep value). Of course, as we saw back in September, as a result of massive crowding and chasing performance, institutional investors have been funneled into growth and momentum stocks and are firmly underweight value and beta.

As Subramanian writes, she analyzed prior inflection points in her regime indicator, from one month prior to inflection through three months into “Early Cycle”, and found that Value fared best (+14.6% avg; 86% hit rate vs. benchmark), but Momentum was weakest (+5.5%, 43% hit rate). And Value beat Momentum during all seven inflection point periods since 1991. In our view, neutralizing Momentum and tilting toward Value is advisable.

BofA’s regime Indicator is just one of several reasons the bank recommends avoiding an anti-Value bias; as noted above, a violent rotation from Momentum to Value started in early September but largely ran its course by mid-month, at which point Momentum stocks resumed leadership. And while value held onto relative gains for the month (6.2%, leading the index by the largest post-crisis monthly margin of +3.1ppt.), in the year-to-date, Value still lags other factors, and investors may have been lulled back into complacency on high momentum stocks.

But as BofA cautions, the unusually low correlations between Momentum and Value, high valuation dispersions and potential for a sharp economic rebound (which however according to Goldman, carries an entirely new set of risks), all warrant a tilt toward Value. But if there is one clear reason why it finally may be “Value’s” time, it is that Value stocks are deeply underweight by active managers (0.89 avg. relative weight in the factor) and BofA’s Value factor screens as inexpensive, trading at a near 25% discount to history on Price to Book Value.

One final reason to expect a violent shift away from momentum and to value is that the calendar provides further support for a Value tilt: based on historical relative 4Q performance back to 1989…

… Value factors tend to outperform most in the 4Q, where Free Cash Flow to Enterprise Value led. Cash Return factors also fare well. But more importantly, growth factors were unequivocally weakest in the 4Q (Long Equity Duration and High EPS Momentum lagged most). Finally, among the notable risk factors, High Beta has outperformed most consistently in the last quarter of the year, providing some evidence for the notion of a year-end beta chase led by institutional investors.

One final word of caution: whereas the relationship between Growth and Value has stabilized in recent weeks, if one lumps all the strategies that were impacted by the September growth/duration/macro reversal as Nomura’s Charlie McElligott has done in the next chart, one can see why virtually nobody is having a good year.

Tyler Durden

Wed, 10/23/2019 – 14:40

![]() Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/T104fuWmKuU/risk-imminent-whipsaws-bofas-regime-indicator-last-month-its-downturn-phase

Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/T104fuWmKuU/risk-imminent-whipsaws-bofas-regime-indicator-last-month-its-downturn-phase