Hertz Is One Recession Away From Bankruptcy

-

Operating income hasn’t covered interest expense since 2015 and the total debt continues to soar.

-

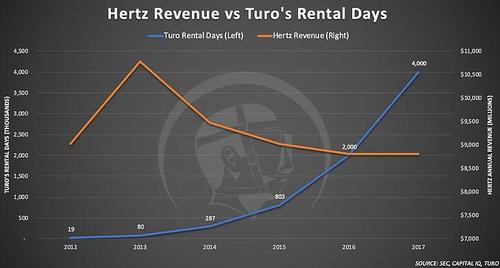

The competition has been pressuring revenue since 2013 and is only getting stronger.

-

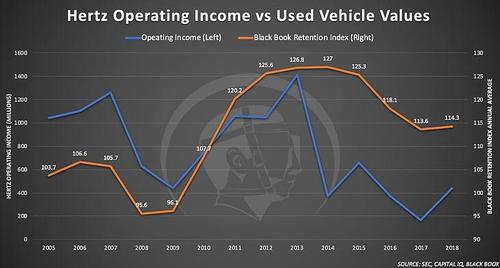

2018 used-vehicle values were as good as it’s going to get.

-

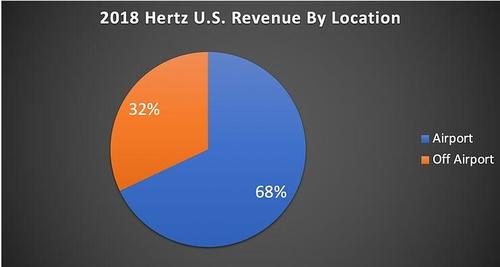

Airline passenger volume falls during recessions and 68% of Hertz’s revenue comes from airport locations.

In a recent interview with Real Vision, I identified Hertz as a good short target. Since the interview, Hertz reported Q4 and full-year earnings (or lack thereof) that were above analyst estimates causing the stock to rally. Most of the improvement that took analysts by surprise was due to the abnormally strong performance in used-vehicle values during 2018 which dropped Hertz’s used-vehicle depreciation per unit by 16% on a year-over-year basis. So is all of the pessimism surrounding Hertz overdone and should the 2018 results be the all-clear signal to buy? Let’s let’s take a closer look.

Used-Vehicle Values

Used-vehicle values play a very important role in the profitability of rental car companies. Put simply, the vehicle expense that rental car companies report is mostly based on the purchase price less the recovery value at disposition. As used-vehicle values increase, the gap between the purchase price and recovery value shrinks which translates into a smaller depreciation amount per vehicle and, under normal conditions, better margins. The opposite happens when used-vehicle values fall. As you can see in the chart below, used-vehicle values and Hertz’s operating income have a strong correlation.

The correlation between operating income and used-vehicle values remained very tight until 2013 (more on this later). As shown by the Black Book Retention Index, used vehicle values have been falling since 2014 and have undoubtedly contributed to the decline in operating income. As I mentioned in my opening statement, used-vehicle values were abnormally high in 2018, and the benefit can be observed by the improvement in operating income.

The big question now is, did 2018 mark a trend change in used-vehicle values or was it a one-time head fake before the downtrend continues? Please click here for a thorough explanation of what drove the strong used-vehicle value performance in 2018 and the likely scenario going forward.

Competition

What I’ve shared with you about used-vehicle values belongs in the expense category, but what about revenue? It’s a well-documented fact that Uber and Lyft have put significant pressure on Hertz’s ability to generate revenue. However, one could argue that rental cars are still more convenient for longer-term use (e.g., multi-day business trips, family vacations, etc). Well, now we a have competitor entering that space as well. Remember, when I said we’d talk later about the tight correlation between used-vehicle values and operating income until 2013? Now is the time. Look at the chart below which compares Hertz’s operating income to Turo’s rental days.

While we can argue that Lyft and Uber might not be direct competitors, it is absolutely undeniable that every Turo transaction represents a transaction lost by traditional rental car companies. Turo is not the only competitor in this space either, GM made it clear that they want a piece of the rental car business when they announced their Maven car sharing service and since then FCA has followed suit.

Crushing Debt

Perhaps one of the best and simplest ways to measure the safety of an investment in a company with debt is by measuring the company’s ability to cover its interest expense with its operating income. The more times over the interest expense is covered by the operating income, the larger the margin of safety should profit fall for unforeseen circumstances.

Hertz’s interest expense has been greater than their operating income for three years in a row, and their total debt continues to soar. Consider what I’ve shared with you so far and ask yourself if this trend is likely to change. What could Hertz possibly do substantially increase revenue and lower expenses in order to pay back their ever-increasing debt over time? If the answer is nothing or not enough, then Hertz is clearly on an unsustainable path.

Revenue Sources

I think I’ve made a strong argument for why even a slight/moderate drop in used-vehicle values combined with the continued pressure from competitors and the ever-increasing interest expense is enough to close the doors at Hertz over time. However, to fully understand the title of this article, it’s important to consider whether Hertz can survive even a mild recession. In 2018, 68% of Hertz’s U.S. revenue came from their airport locations.

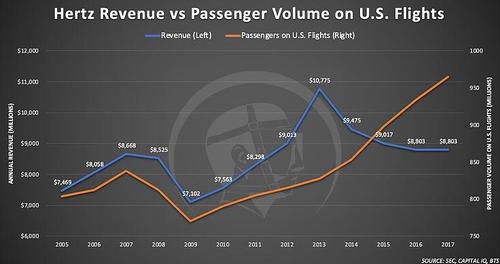

Offsetting some of the pressure from recent competition has been a strong and consistent increase in passenger volume of U.S. flights.

As you can see in the chart above, airline passenger volume falls during a recession. Due to the large percentage of revenue that Hertz generates at airports (strong correlation between revenue and passenger volume on U.S. flights before the current onslaught of competition), we can assume that where airline passenger volume goes, Hertz’s revenue will follow. The decline in revenue from 2013 was due to competition, but it was partially offset by strong and steady growth in airline passenger volume. That thought leads us to the next question, can Hertz avoid bankruptcy in a recession where airline passenger volume is likely to drop and used-vehicle values are likely to fall? My guess is no.

Folks, if I’ve failed to explain my view on why Hertz is a good short, I hope that I’ve at least succeeded in showing you why it’s a terrible investment. The stock is very volatile so it’s not impossible to play a game of hot potato profitably from the long side (I don’t recommend it). Hertz can certainly rally as some metrics improve due to market conditions that are completely beyond the company’s control, just don’t be the last one holding the potato when the music stops.

![]() Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/oYrcXVLrRi8/hertz-one-recession-away-bankruptcy

Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/oYrcXVLrRi8/hertz-one-recession-away-bankruptcy