Is Global Manufacturing Staging A Comeback?

Is Global Manufacturing Staging A Comeback?

Authored by Chetan Ahya, chief economist and global head of economics at Morgan Stanley

What was your defining moment of 2019? For the global economy, it would have to be the recessionary conditions in the manufacturing and trade sectors and their drag to global growth. The good news? As we enter 2020, these sectors are staging a comeback.

Consider the recent run of both soft and hard data. In November, the soft data, most notably the manufacturing PMIs, improved for the first time in seven months. In December, both the headline and new orders index held on to their previous month’s values, as the further improvement in PMIs in EM was offset by weaker PMIs in DMs, particularly the US.

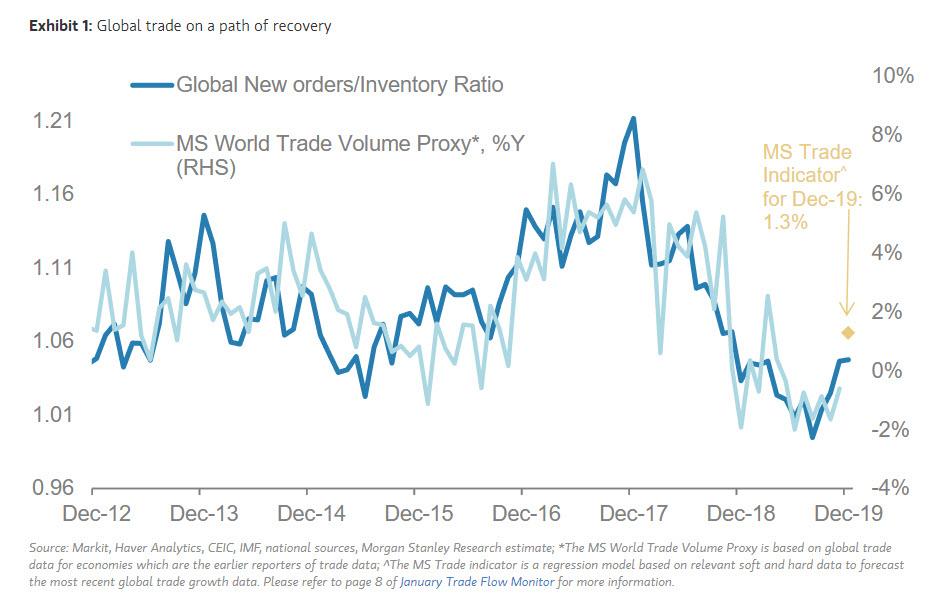

Encouragingly, the bounce in the soft data in November has translated to an uptick in the hard data for December. Korea’s exports volume – the first real-time indicator for global trade – returned to a positive growth rate of 6.9%Y in December, after contracting for the past seven months. Similarly, we estimate that global trade, as per our trade indicator, is likely to post 1.3%Y growth in December, the first month of positive growth after seven months of contraction.

We have reasons to believe that this improvement in manufacturing and trade can be sustained.

- First, trade tensions are easing. On current indications, a phase 1 deal between the US and China is likely to be signed on January 15. As further escalation is averted, this reduces the drag from a key overhang on corporate confidence. Moreover, the global economy received a substantial amount of monetary and fiscal stimulus and its effects are kicking in now to support end demand.

- Second, the weakness in global manufacturing and trade was exacerbated by the inevitable inventory adjustment that corporates had to undertake in response to weak demand conditions. However, judging by the current low levels of inventory, we believe that the inventory adjustment cycle is nearly complete in China and Europe (the two big manufacturing hubs). Globally, the new orders to inventory ratio for the manufacturing PMIs has rebounded sharply over the last four months.

At a micro level, the turnaround in the Asia tech cycle provides another avenue of optimism. The tech sector accounts for a sizeable share in Asia excluding Japan manufacturing, and Asia excluding Japan accounts for ~40% of global manufacturing. Shawn Kim, our head of Asia technology research, is highlighting that many tech verticals, including global semis, DRAM, display panels and smartphones to name a few, are inflecting higher in terms of their year-on-year rate of change, which Shawn believes marks a fundamental cyclical upturn. As tech is a big part of global manufacturing, its improvement, even if it is driven by sector-specific reasons, will support a recovery in global manufacturing.

To be sure, this rising tide of better growth in manufacturing and trade will help to lift global growth, but not all economies will benefit to the same extent. Compared with the rest of the world, the US has a smaller exposure to these sectors. Hence, we expect a more robust growth recovery in the world excluding the US. The US economy is also constrained by late-cycle dynamics while resources are less stretched elsewhere.

At the same time, the effects of policy support are fading in the US but policy easing is gaining momentum elsewhere. Fiscal policy is turning more supportive of growth in the euro area, Japan and the UK. In China, as trade tensions ease and corporate confidence improves, it will increase the effectiveness of the tax cuts. Moreover, policy-makers are continuing their push to support growth with the increase in the annual quota of local government special bond issuance for 2020, which is likely to be front-loaded.

As the upturn in trade and manufacturing continues, it should provide an upswing to the global economy. We expect global GDP growth to improve from a trough of 2.9%Y in 4Q19 to 3.4%Y in 4Q20, driven by a more robust improvement in the rest of the world. The risks to the recovery will be if trade tensions between the US and China escalate again, a rise in geopolitical tensions in the Middle East or if late-cycle challenges in the US – for instance, if financial stability risks rise or there is a much sharper acceleration of wage growth relative to capex and productivity growth – result in a more pronounced rise in inflation. In this context, the Fed’s reaction to these scenarios playing out would be key, as it could prompt an earlier-than-expected rate hike by the Fed (relative to our expectation of an extended hold in 2020).

Enjoy your Sunday. On behalf of all my colleagues at Morgan Stanley Research, we wish you a happy new year.

Tyler Durden

Sun, 01/05/2020 – 17:00

![]() Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/eEUWk5pUa1Q/global-manufacturing-staging-comeback

Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/eEUWk5pUa1Q/global-manufacturing-staging-comeback