Is This Why Elon Musk Is Talking Down His Stock Price

Is This Why Elon Musk Is Talking Down His Stock Price

Submitted by Gordon Johnson of GLJ Research

In our view, TSLA desperately needs money now; yet, at ~$700/shr, there’s limited demand from institutional investors for the type of raise ($4-$5bn) they need to do. So… Elon Musk needs to get the stock price down before he potentially trips debt (etc.) covenant levels on actual cash on hand, or has to issue a going concern alert.

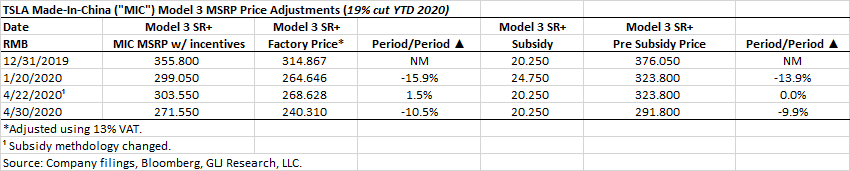

Every week Fremont is down, TSLA burns $300mn. And, based on reports from the Chinese media, GF3 (i.e., TSLA’s Shanghai plant) sources just 30% of its parts from Chinese producers (the rest come from Fremont). We’re hearing, from credible checks, that the China Communist Party (“CCP”) is becoming “agitated” by TSLA’s delays to source more parts from Chinese companies (i.e., TSLA is bidding too low); and, as a result, the CCP is pushing TSLA to big price cuts, again, on made-in-China (“MIC”) SR+/LR models as soon as July (apparently, this is being pushed by CCP ministries) – TSLA has already cut the price on it’s MIC Model 3 SR+ car by -23.7% YTD.

Thus, with the shelter-in-place in Almeda County (where TSLA’s GF2 is located) extended to June, TSLA may need to idle it’s Shanghai plant in June. We est. this would cost TSLA ~$150mn/week.

Along these lines… with Fremont down 4 weeks, or (4 * $300mn = $1.2bn), and Shanghai down an est’d ~2 weeks in June, or (2 * $150mn = $300mn), the total cost of all this is around $1.5bn. However, in 1Q20, TSLA reported $8bn in cash vs. $4bn in payables (i.e., half the cash is due in payables). And, TSLA burnt -$895mn in FCF in 1Q20, alone. So, with their plants shut, they will likely have to pay a LOT of those payables over the course of 2Q20 (they admitted, on their call, that they delay payments to their suppliers to the forward quarter, and, given they won’t be able to do that this qtr [as they are not making cars], they will likely see a large drop in the payable balance).

Consequently… the cash balance could drop to: $8bn (at end of 1Q20) – $1.5bn – $4bn – $1.2bn (FCF burn associated with less cars made in 2Q20 vs. 1Q20) = $1.3bn in 2Q20 without a raise.

In our view, TSLA desperately needs money now

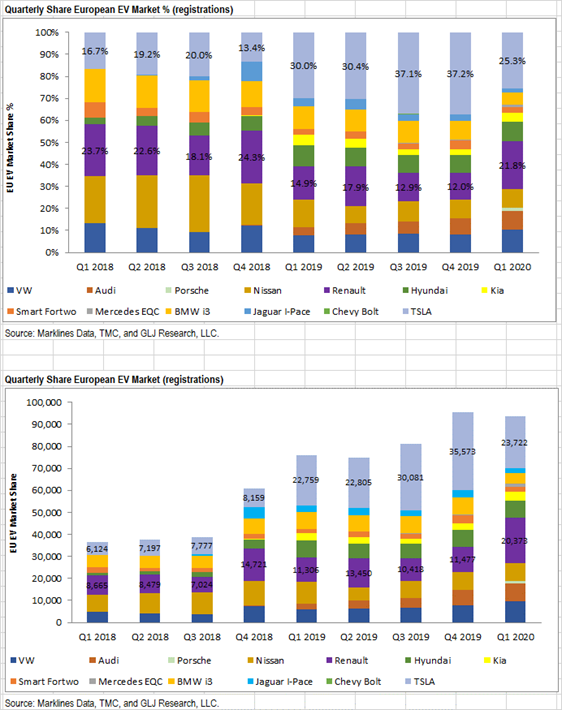

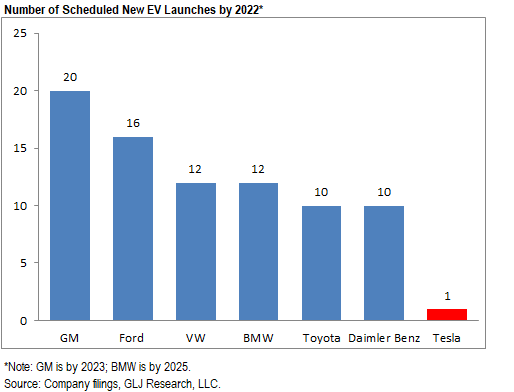

A few charts for your viewing pleasure:

* * *

There is another, somewhat more conspiratorial if no less credible , theory floating around summarized best by investor Rob Schmied:

2/ Share sales raising billions could only take a few days prior to the required SEC filings disclosing such sales. His tweets today arguably gave everyone fair warning of these pending sales (“selling almost all physical possessions”). Shares are physical possessions.

— Rob Schmied (@rschmied) May 1, 2020

4/ It is now common knowledge that EM is selling his possessions and thinks the shares are overvalued.

How can anyone sue? Furthermore, his tweets might result in his dismissal as CEO in the very near term (30 days?). Provides enough time to clean up any internal smoking guns.— Rob Schmied (@rschmied) May 1, 2020

6/ So in summary, EM gets billions out while telling everyone he is doing it, the company will ultimately go BK and can blame COVID-19 the fascist behavior of the government, and his persona will likely keep him out of prison and comfortably in his G650.

— Rob Schmied (@rschmied) May 1, 2020

8/ Lastly, I believe he is still restricted from selling pursuant to the last equity offering, until May 13th. This can be waived by GS however. Perhaps GS asked him to “disclose” via twitter that he was selling and that the shares were pricey? all jmho and pure speculation.

— Rob Schmied (@rschmied) May 1, 2020

Tyler Durden

Fri, 05/01/2020 – 18:25![]() Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/wDIjpI4D4IM/why-elon-musk-talking-down-his-stock-price

Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/wDIjpI4D4IM/why-elon-musk-talking-down-his-stock-price