“The Market Is On Thin Ice”: Have Stocks Sucessfully Averted A Crisis?

Having warned about a potential “Lehman-like shock” as recently as the first week of August, Nomura’s quant team has turned decidedly more sanguine on the risk of an imminent market crash with stocks failing to take out new lows in recent weeks despite a daily rollercoaster in risk sentiment. And while on 1 September, the US and China went ahead with planned tariff hikes on goods imported from one another – contrary to some more optimistic market expectations – this has not had much of a market impact as of yet, although E-mini S&P 500 futures did drop to around 2,900.

So with risk assets able to absorb virtually any development geopolitics can throw at them, Nomura’s Masanari Takada asks if a (Lehman-like) crisis been successfully averted in global equity markets?

His answer is that, while the market is still on shaky ground however, the signs last week that the US and China might make some mutual concessions—along with the health of the incoming US macroeconomic data—may have blunted the attack on the downside that some speculative traders had been waging. Trend-chasing investors in particular, after perhaps going a little too far with pessimistic trades (selling stocks, buying bonds), seem to have been forced into cooling off a bit after running out of patience.

As Takada admits, in recent weeks (documented here) his team expressed concern that the stock market was heading for “a moment of truth” by around 2 September, based on the pattern we observed in market sentiment. Through 30 August, however, sentiment had not experienced any sort of profound collapse and, if anything, expectations for progress in US-China trade negotiations may have kept sentiment from deteriorating. That said, it is worth noting that that alternating positive and negative headlines on the US-China standoff have lured the market into a series of swings between optimism and pessimism, and as Nomura warns “the present state of sentiment may be another example of expectations getting ahead of reality,” although since it remains a largely event-driven market at the moment, “if sentiment manages to hold up well when the market opens after the Labor Day holiday, it would mark a break (in a good way) from the trajectory that it would follow if it were to stick to the historical pattern.”

How are the main players positioned?

In terms of supply and demand among speculative traders, Nomura had been expecting CTAs to step up their net selling of equity futures, possibly taking the S&P 500 down to below 2,800 by the time they had closed out the entirety of their net long position. As it happened, however, CTAs were ultimately forced into calling a halt to their pessimistic trades last week, “as global macro hedge funds went in a decidedly un-pessimistic direction with an unexpected acceleration in their stock buying and bond selling.”

The improvement in macroeconomic indicators (economic surprise indices) surely goes at least some of the way to explaining the investment behavior of global macro hedge funds last week. Some other key US macroeconomic indicators are due for release when the market returns from the Labor Day holiday, and somewhat ominously and seasonally speaking, this is when improvement tends to stall, which is when Takada says, it will be interesting to see whether global macro hedge funds press ahead with their optimistic stance.

What tends to happen after Labor Day?

Looking to the immediate horizon, Nomura notes that it is possible that the unwinding of some pessimistic trades by CTAs will systematically trigger a risk-on mood. However, a lingering risk is that global macro hedge funds may be due for a reality check. Global macro hedge funds look isolated in their bullishness; other speculative traders appear less than eager to take on risk.

Here, Nomura warns that it has yet to see any of the developments that it has identified as potential game changers (a US-China trade agreement, a virtual promise by the Fed to cut interest rates significantly, or the emergence of coordinated fiscal action), and for that reason “the market as a whole is on thin ice.” It’s also why the bank’s recommendation would be to sell rallies, for example if the S&P 500 were to close at an intraday high short of 2,960.

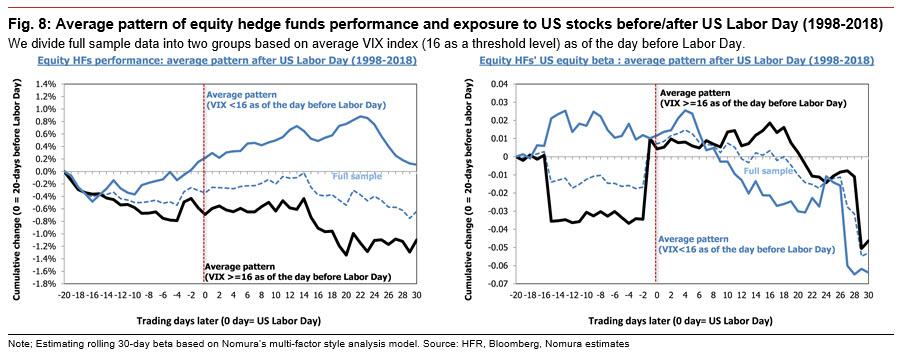

Finally, in terms of seasonal patterns, after going over the data since 1990 on how various market measures (US stock indices, 10yr UST yields, DXY, gold) tend to perform when the market re-opens after the Labor Day holiday, Nomura found that when the average VIX reading over the course of August has been above the warning sign level of 16 (as is true of this year’s 19.1), the risk-off momentum tends to linger across multiple asset classes after the market returns from the long Labor Day weekend.

The historical behavior of long/short funds also deserves mention here. When markets have been turbulent in August, long/short funds have tended to rebuild their equity exposure right around Labor Day, but their bullishness has typically turned out to be short-lived. At the very least, Nomura’s quant team – cautious as always – thinks that “investors should take the view that hedge funds will accelerate their stock buying after the Labor Day holiday with a grain of salt.”

![]() Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/ILE3xeozl_s/market-thin-ice-have-stocks-sucessfully-averted-crisis

Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/ILE3xeozl_s/market-thin-ice-have-stocks-sucessfully-averted-crisis