“VIX Is Unusually Low” – Goldman Warns, It’s A Big Week In The Vol Complex

Since credit and equity risk expectations exploded amid the Mnuchin Massacre on Xmas Eve, PPT-enabled liquidity, The Fed folding on its normalization agenda, and a constant line of propaganda that a China “deal” is close has prompted the collapse of market participants’ views of uncertainty going forward…

In fact, as stocks rose, VIX has collapsed considerably more…

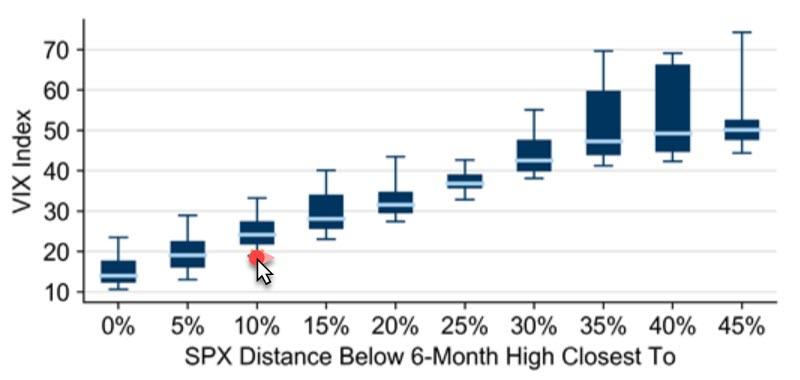

And as Goldman Sachs says, VIX is unusually low in the context of an SPX that’s still 10% below its peak…

Distribution of VIX levels based on how far below its 6-month high the SPX is (since 1993; box plot shows 5/25/50/75/95th percentiles)

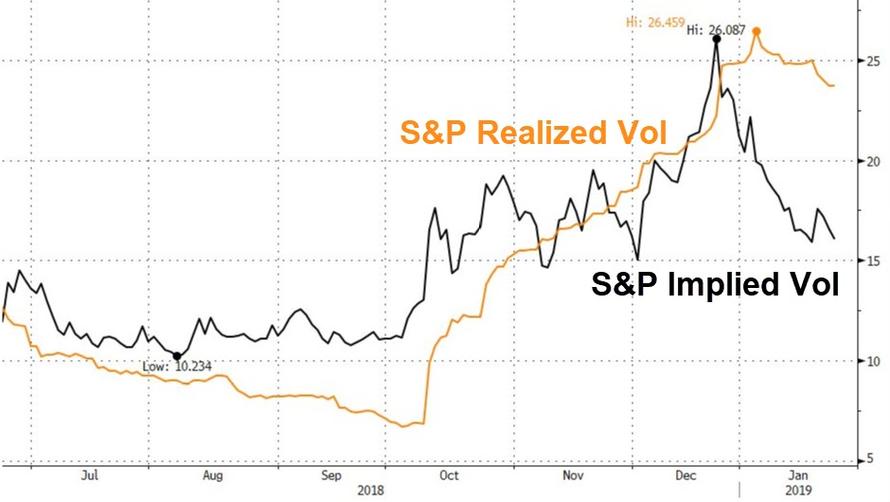

…and also relative to realized volatility.

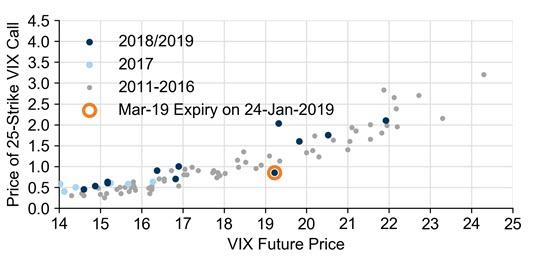

And, with weakened liquidity as an ongoing risk factor for an escalation in volatility, Goldman sees VIX calls as good value.

We recommend: Buy Mar-2019 25-strike VIX calls for $0.85 (indic. mid, ref. fut. 19.2). The 25 strike is roughly 25-delta, and the (Tuesday) 19-Mar-19 maturity is soon after the deadline for escalating tariffs with China.

VIX call prices unusually low for the current futures level

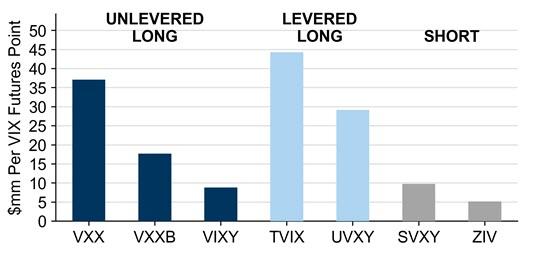

However, they suspect the timing may be better after Tuesday, because with the VXX maturing next week, it remains the largest VIX ETP and has around $700mm of AUM.

On Tuesday, the VXX exchange-traded note will reach its final valuation date, at which point the note will cease to trade and holders of it will receive a cash payment representing the note’s NAV. To date, only the minority of the VXX’s AUM has rolled to competing products (the largest products with nearly identical economics are the VXXB and VIXY).

Exhibit 5: VXX continues to represent a large percentage of outstanding VIX ETP vega

Current vega outstanding ($mm per VIX futures point) in largest US-listed VIX ETPs

If a substantial amount of VXX shares do not switch to comparable products, the note’s issuer could have a large, but not unmanageable, amount of VIX futures to sell at Tuesday’s close, putting pressure on the February and March VIX futures.

Although the VXX has continued to have much higher trading volume and liquidity metrics than the VXXB or VIXY, with only one VXX option maturity remaining, this week VXXB option volume has caught up with VXX option volume. There are now VXXB options listed through Jan-2021, allowing investors to return to trade options on long-dated SPVXSP risk (essentially risk-limited views on how steep or inverted the implied volatility curve will be over the next 1-2 years).

The growth in institutional-sized VXXB option trades is an indication that institutional investors are beginning to accept the product as a substitute for the VXX.

* * *

So, all in all, this week could be a big one for the vol complex – aside from headline event risk from The Fed, the final death of the VXX ETF could mean some crazy VIX-futures-driven tails wagging the market’s dog.

![]() Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/owm9aY3K_fs/vix-unusually-low-goldman-warns-its-big-week-vol-complex

Original source: http://feedproxy.google.com/~r/zerohedge/feed/~3/owm9aY3K_fs/vix-unusually-low-goldman-warns-its-big-week-vol-complex